Morgan Stanley: The End of Fed QT ≠ Restart of QE, Treasury's Issuance Strategy Is the Key

Morgan Stanley believes that the end of the Federal Reserve's quantitative tightening does not mean a restart of quantitative easing.

Morgan Stanley believes that the end of the Federal Reserve's quantitative tightening does not mean a restart of quantitative easing.

Written by: Long Yue

Source: Wallstreetcn

The Federal Reserve's decision to end quantitative tightening (QT) has sparked widespread discussion in the market regarding a potential policy shift, but investors should not simply equate this move with the start of a new round of monetary easing.

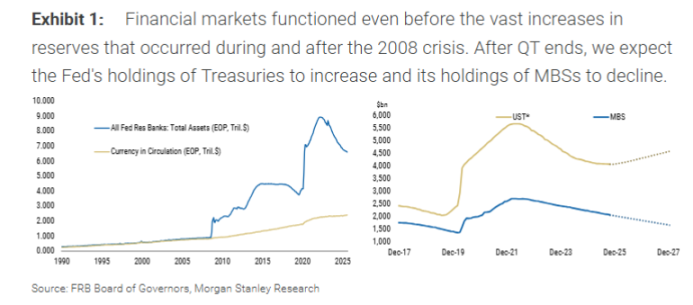

According to a Morgan Stanley report, the Federal Reserve announced at its most recent meeting that it will end quantitative tightening on December 1. This action is about six months earlier than the bank previously expected. However, its core mechanism is not the "flood of liquidity" that the market anticipates.

Specifically, the Federal Reserve will stop reducing its holdings of Treasury securities, but will continue to allow about $15 billion of mortgage-backed securities (MBS) to mature and roll off its balance sheet each month. At the same time, the Fed will purchase an equivalent amount of short-term Treasury bills (T-bills) to replace these MBS.

The essence of this operation is an asset swap, not an increase in reserves. Morgan Stanley's Chief Global Economist Seth B Carpenter emphasized in the report that the core of this operation is to change the "composition" of the balance sheet, not to expand its "size." By releasing the duration and convexity risk associated with MBS to the market while purchasing short-term debt, the Fed is not substantially loosening financial conditions.

Ending QT Does Not Equal Restarting QE

The market needs to clearly distinguish this operation from quantitative easing (QE). QE aims to inject liquidity into the financial system through large-scale asset purchases, thereby lowering long-term interest rates and easing financial conditions. The current Fed plan, however, is merely an internal adjustment of its asset portfolio.

The report points out that the Fed's replacement of maturing MBS with short-term Treasury bills is a "security swap" with the market and does not increase reserves in the banking system. Therefore, interpreting this as a restart of QE is a misunderstanding.

Morgan Stanley believes that although the Fed's decision to end QT early has attracted significant market attention, its direct impact may be limited. For example, stopping the $5 billion monthly reduction in Treasuries six months early results in a cumulative difference of only $30 billion, which is negligible compared to the Fed's massive portfolio and the overall market.

Future Balance Sheet Expansion Is Not "Liquidity Injection": Only to Hedge Cash Demand

So, when will the Fed's balance sheet expand again? The report suggests that, barring extreme situations such as a severe recession or financial market crisis, the next expansion will be for a "technical" reason: to hedge the growth of physical currency (cash).

When banks need to replenish cash for their ATMs, the Fed provides banknotes and correspondingly deducts from the bank's reserve account at the Fed. Therefore, the growth of cash in circulation naturally consumes bank reserves. Morgan Stanley predicts that in the coming year, in order to maintain stable reserve levels, the Fed will begin purchasing Treasuries. At that time, the scale of Fed bond purchases will increase by an additional $1 billion to $1.5 billion per month on top of the $1.5 billion used to replace MBS, to match the reserve loss caused by cash growth.

The report emphasizes that the sole purpose of such bond purchases is to "prevent a decline in reserves," not to "increase reserves," and thus should not be over-interpreted by the market as a signal of monetary easing.

The Real Key: Treasury's Debt Issuance Strategy

Morgan Stanley believes that for asset markets, the real focus should shift from the Fed to the US Treasury Department.

The report analyzes that the Treasury is the key player in determining how much duration risk the market needs to absorb. The Treasuries reduced by the Fed ultimately return to the market through new issuance by the Treasury. The Treasury's recent strategy has been to increase the issuance of short-term bonds. The Fed's purchase of short-term Treasuries may facilitate the Treasury's further increase in short-term issuance, but this is entirely dependent on the Treasury's final decision.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

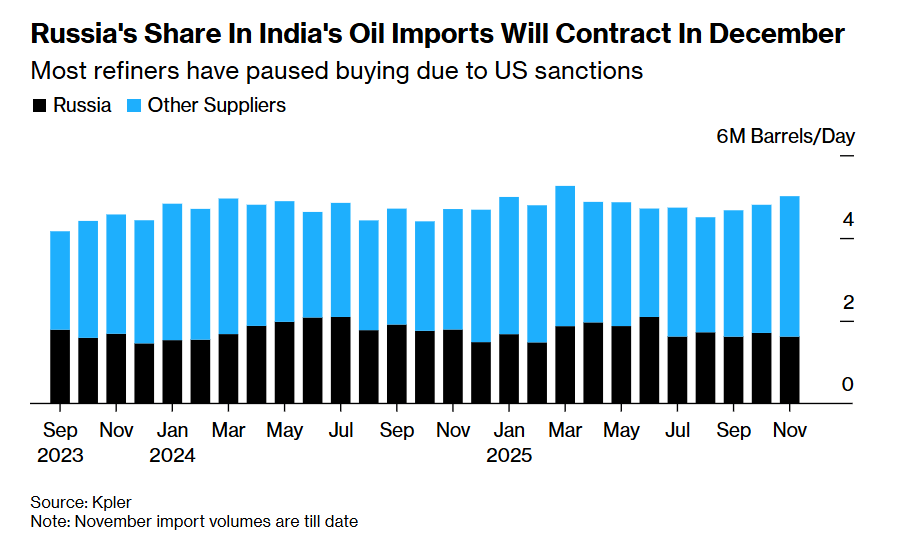

Trump's pressure works! India's five major refineries suspend orders for Russian oil

Due to Western sanctions and US-India trade negotiations, India significantly reduced its purchases of Russian crude oil in December, with its five major core refineries placing no orders.

Masayoshi Son takes action! SoftBank sells all its Nvidia shares, cashing out $5.8 billions to shift towards other AI investments

SoftBank Group has completely sold its Nvidia holdings, cashing out $5.8 billions. Founder Masayoshi Son is shifting the strategic focus, allocating more resources to the artificial intelligence and chip-related sectors.

Research Report|In-Depth Analysis and Market Cap of Allora Network (ALLO)

CryptoQuant: Stablecoin reserves reach all-time highs, Bitcoin may be poised for a new surge.