Written by: Alex Krüger

Translated by: Block unicorn

Preface

The Federal Reserve as we know it will end in 2026.

The most important driver of asset returns next year will be the new Federal Reserve, especially the regime change brought by Trump's new Fed chair.

Hassett has become Trump's top pick to lead the Federal Reserve (with a 71% probability on Polymarket). Currently serving as the Director of the National Economic Council, he is a supply-side economist and a long-time loyal supporter of Trump, advocating a "growth-first" philosophy. He believes that, with the anti-inflation war essentially won, maintaining high real interest rates is a matter of political stubbornness rather than economic prudence. His potential appointment marks a decisive regime shift: the Federal Reserve will move away from the technocratic caution of the Powell era, shifting to a new mission that clearly prioritizes lowering borrowing costs to advance the president's economic agenda.

To understand the policy framework he would implement, let's accurately assess his statements this year regarding interest rates and the Federal Reserve:

-

"The only explanation for the Fed not cutting rates in December is anti-Trump partisan bias." (November 21)

-

"If I were on the FOMC, I would be more likely to cut rates, while Powell would be less likely to do so." (November 12)

-

"I agree with Trump that rates could be much lower." (November 12)

-

"The expected three rate cuts are just the beginning." (October 17)

-

"I hope the Fed continues to cut rates significantly." (October 2)

-

"The Fed's rate cuts are a step in the right direction toward much lower rates." (September 18)

-

"Waller and Trump are right about rates." (June 23)

On a dovish-to-hawkish scale of 1-10 (1 = most dovish, 10 = most hawkish), Hassett scores a 2.

If nominated, Hassett will replace Milan as a Fed governor in January, when Milan's short-term tenure ends. Then in May, when Powell's term ends, Hassett will be promoted to chair. Following historical precedent, Powell, after announcing his intentions months in advance, will resign from the remaining governor seat, paving the way for Trump to nominate Walsh to fill the position.

Although Walsh is currently Hassett's main competitor for the chair nomination, my core assumption is that he will be included in the reformist camp. As a former Fed governor, Walsh has been "campaigning" on a platform of structural reform, explicitly calling for a "new Treasury-Fed accord" and criticizing the Fed leadership for succumbing to "the tyranny of the status quo." Crucially, Walsh believes that the current AI-driven productivity boom is inherently deflationary, meaning that the Fed's maintenance of restrictive rates is a policy mistake.

A New Balance of Power

This setup will give Trump's Federal Reserve a strong dovish core and credible voting influence on most easing decisions, though this is not guaranteed, and the degree of dovish tilt will depend on consensus.

-

Dovish core (4 people): Hassett (Chair), Walsh (Governor), Waller (Governor), Bowman (Governor).

-

"Persuadable centrists" (6 people): Cook (Governor), Barr (Governor), Jefferson (Governor), Kashkari (Minneapolis), Williams (New York), A. Paulson (Philadelphia).

-

Hawks (2 people): Harker (Cleveland), Logan (Dallas).

However, if Powell does not resign from the governor seat (which is highly likely; historically, all outgoing chairs have resigned, e.g., Yellen resigned 18 days after Powell's nomination), it would be extremely bearish. This move would not only block the vacancy needed for Walsh but also make Powell a "shadow chair," forming another potentially more loyal power center outside the dovish core.

Timeline: Four Phases of Market Reaction

Considering all the above, the market reaction should be divided into four distinct phases:

There will be immediate optimism about Hassett's nomination (December) and bullish sentiment in the weeks following confirmation, as risk assets will love having a high-profile dovish loyalist as chair.

If Powell does not announce his resignation from the board within three weeks, anxiety will grow, as each day that passes raises the question, "What if he refuses to leave?" Tail risks will re-emerge.

The moment Powell announces his resignation, there will be a wave of euphoria.

As the first FOMC meeting led by Hassett approaches in June 2026, the market will become nervous again, closely watching every word from FOMC voting members (who speak regularly, offering glimpses into their views and thought processes).

Risk: A Divided Committee

Since the chair does not have the "deciding vote" many imagine (in fact, there is none), Hassett must win the debate within the FOMC to secure a true majority. Every 50-basis-point move could result in a 7-5 split, which would cause institutional damage by signaling to the market that the chair is a political operator rather than an impartial economist. In extreme cases, a 6-6 tie or a 4-8 vote against rate cuts would be disastrous. The exact vote count will be published in the FOMC minutes three weeks after each meeting, turning these releases into major market-moving events.

What happens after the first meeting is the biggest unknown. My base case is that if Hassett secures four solid votes and has a reliable path to ten, he will forge a dovish consensus and execute his agenda.

Inference: The market cannot fully front-run the Fed's new dovish stance.

Rate Repricing

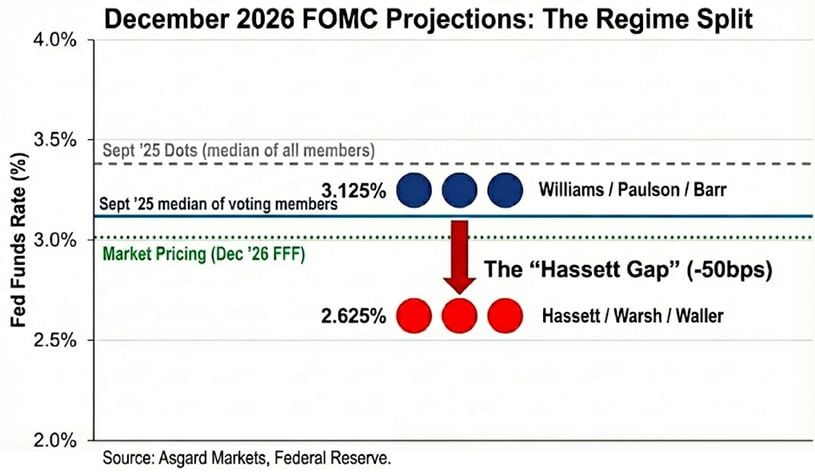

The dot plot is just an illusion. Although the September dot plot projected a 3.4% rate for December 2026, this figure represents the median of all participants, including hawks who do not vote. By anonymizing the dot plot based on public statements, I estimate the median among voters is much lower, at 3.1%.

When I substitute Hassett and Walsh for Powell and Milan, the situation changes further. If Milan and Waller represent the new Fed's aggressive rate-cutting stance, the 2026 voting distribution remains bimodal, but with a lower peak: Williams / Paulson / Barr at 3.1%, Hassett / Walsh / Waller at 2.6%. I anchor the new leadership's rate at 2.6%, matching Milan's official forecast. However, I note that he has expressed a preference for a "neutral rate" of 2.0% to 2.5%, suggesting the new regime's bias may be even lower than their forecast.

The market has partially recognized this; as of December 2, the expected rate for December 2026 is 3.02%, but it has not fully priced in the extent of this regime change. If Hassett successfully guides rates lower, the short end of the yield curve will need to drop another 40 basis points. Moreover, if Hassett's forecast of supply-side deflation is correct, inflation will fall faster than the market broadly expects, prompting even larger rate cuts to prevent passive tightening.

Cross-Asset Impact

Although the initial reaction to Hassett's nomination should be "risk appetite rises," the true manifestation of this regime change is "steepening inflation"—betting on aggressive easing in the short term but expecting higher nominal growth (and inflation risk) in the long run.

Interest rates: Hassett wants the Fed to cut rates aggressively during recessions while maintaining growth above 3% during booms. If he succeeds, the 2-year Treasury yield should drop sharply to reflect rate-cut expectations, while the 10-year yield may remain high due to structurally higher growth and persistent inflation premium.

Stocks: Hassett believes the current policy stance is actively suppressing the AI-driven productivity boom. He will sharply lower the real discount rate, causing growth stock multiples to "soar." The danger is not recession, but bond market turmoil triggered by a surge in long-end yields in protest.

Gold: A politically unified Fed that clearly puts economic growth above the inflation target is undoubtedly a textbook bullish scenario for hard assets. As the market hedges against the risk of the new administration repeating the policy mistakes of the 1970s through excessive rate cuts, gold should outperform US Treasuries.

Bitcoin: Under normal circumstances, bitcoin would be the purest expression of the "regime change" trade. However, since the shock on October 10, bitcoin has shown severe downside skew, with weak macro rebound momentum and sharp drops on any negative news, mainly due to heightened concerns about the "four-year cycle" and a crisis of bitcoin's own positioning. I believe that by 2026, Hassett's monetary policy and Trump's deregulation agenda will overcome the currently dominant self-fulfilling bearish sentiment.

Technical Note: The "Tealbook"

The Tealbook is the Fed staff's official economic forecast and the statistical benchmark for all Federal Open Market Committee (FOMC) discussions. This report is produced by the Research and Statistics Division, led by Director Tevlin, which has over 400 economists. Like most of her staff, Tevlin is a Keynesian, and the Fed's main model (FRB/US) explicitly adopts New Keynesianism.

Hassett could use a board vote to appoint a supply-side economist to lead the division. Replacing a traditional Keynesian economist (who believes economic growth leads to inflation) with a supply-sider (who believes the AI boom is deflationary) would significantly change the forecasts. For example, if the division's model predicts inflation will fall from 2.5% to 1.8% due to higher productivity, even less dovish FOMC members may be more willing to vote for large rate cuts.