With capital outflows from crypto ETFs, can issuers like BlackRock still make good profits?

BlackRock's crypto ETF fee revenue has dropped by 38%, and its ETF business is struggling to escape the cyclical curse of the market.

Original Title: When Wrappers Run Red

Original Author: Prathik Desai, Token Dispatch

Translated by: Luffy, Foresight News

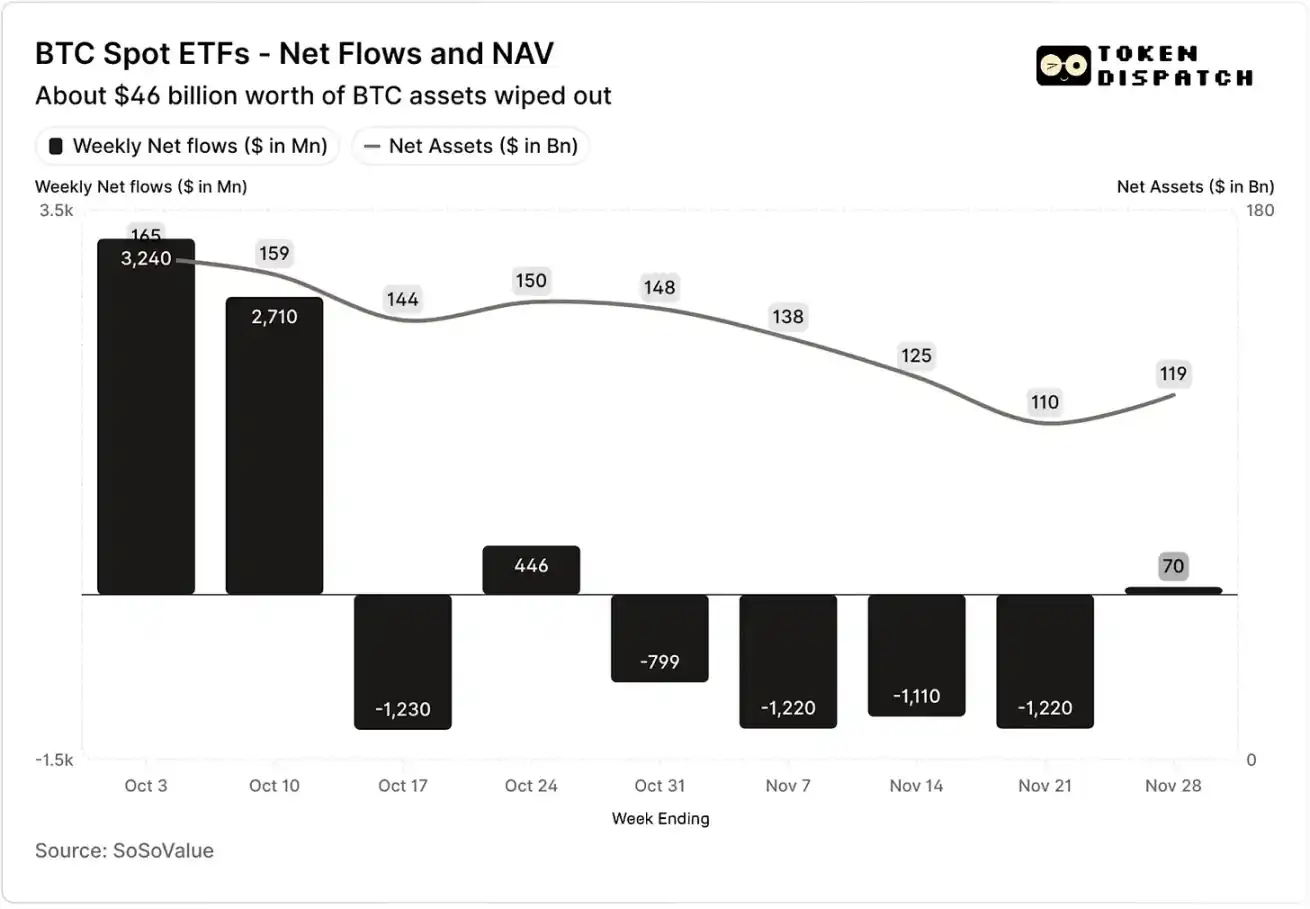

In the first two weeks of October 2025, spot bitcoin ETFs attracted inflows of $3.2 billion and $2.7 billion respectively, setting the highest and fifth-highest weekly net inflow records for 2025.

Before this, bitcoin ETFs were expected to achieve a "no consecutive weeks of net outflows" record in the second half of 2025.

However, the most severe crypto liquidation event in history arrived unexpectedly. This $19 billion asset wipeout still leaves the crypto market with lingering fears.

Net inflows and net asset value of spot bitcoin ETFs in October and November

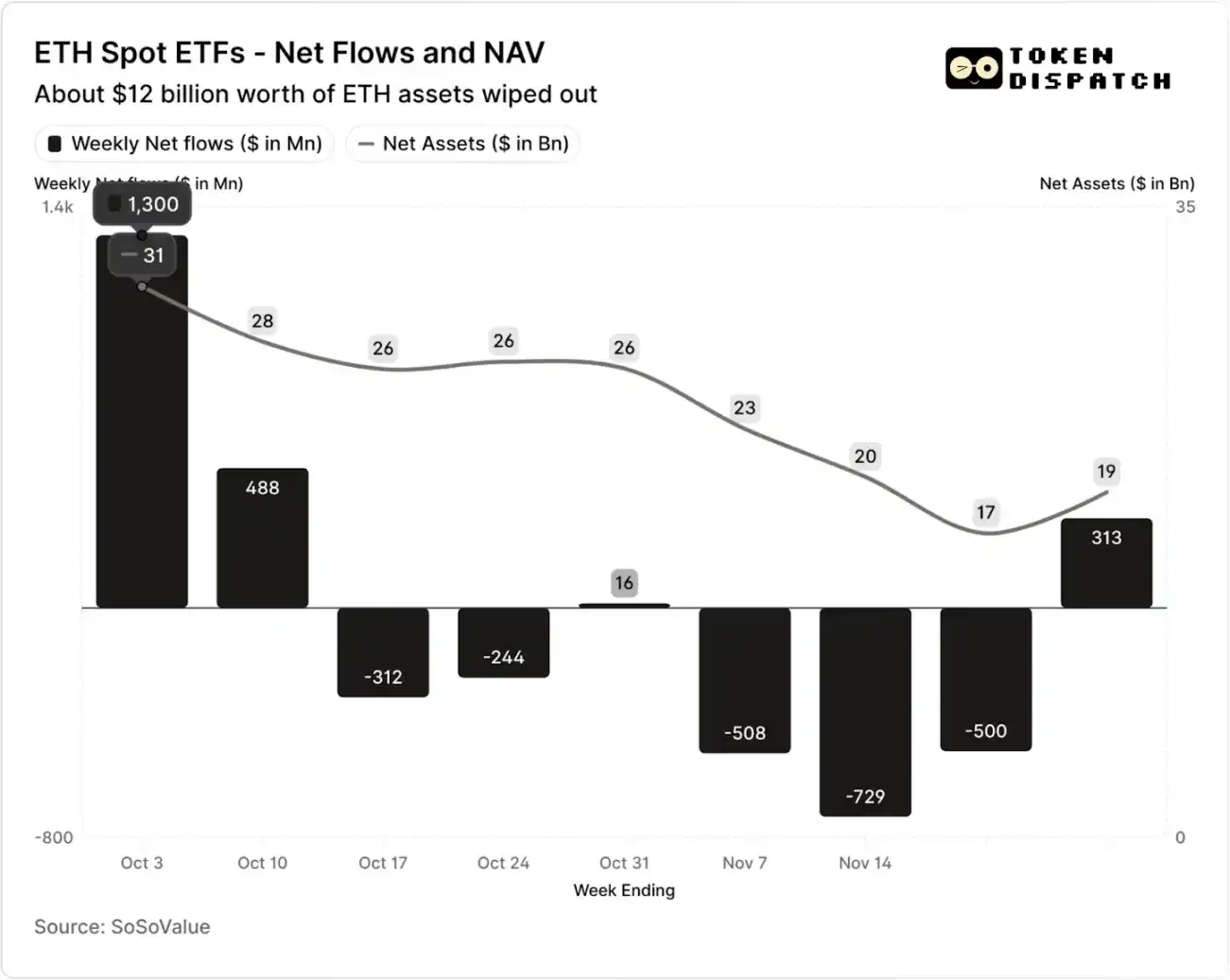

Net inflows and net asset value of spot ethereum ETFs in October and November

But in the seven weeks following the liquidation event, bitcoin and ethereum ETFs experienced outflows in five weeks, with outflows exceeding $5 billion and $2 billion respectively.

As of the week ending November 21, the net asset value (NAV) of assets managed by bitcoin ETF issuers shrank from about $164.5 billion to $110.1 billion; the NAV of ethereum ETFs was nearly halved, dropping from $30.6 billion to $16.9 billion. This decline was partly due to the price drop of bitcoin and ethereum themselves, as well as some tokens being redeemed. In less than two months, the combined NAV of bitcoin and ethereum ETFs evaporated by about one third.

The pullback in capital flows reflects not only investor sentiment but also directly affects the fee income of ETF issuers.

Spot bitcoin and ethereum ETFs are "money printers" for issuers such as BlackRock, Fidelity, Grayscale, and Bitwise. Each fund charges fees based on the scale of assets held, usually announced as an annual rate but actually calculated daily based on NAV.

Every day, the trust funds holding bitcoin or ethereum shares sell a portion of their holdings to pay fees and other operating expenses. For issuers, this means their annual revenue is roughly equal to assets under management (AUM) multiplied by the fee rate; for holders, this leads to a gradual dilution of the number of tokens they hold over time.

The fee rate range for ETF issuers is between 0.15% and 2.50%.

Redemptions or outflows themselves do not directly cause issuers to profit or lose, but outflows will ultimately reduce the scale of assets managed by issuers, thereby reducing the asset base from which fees can be collected.

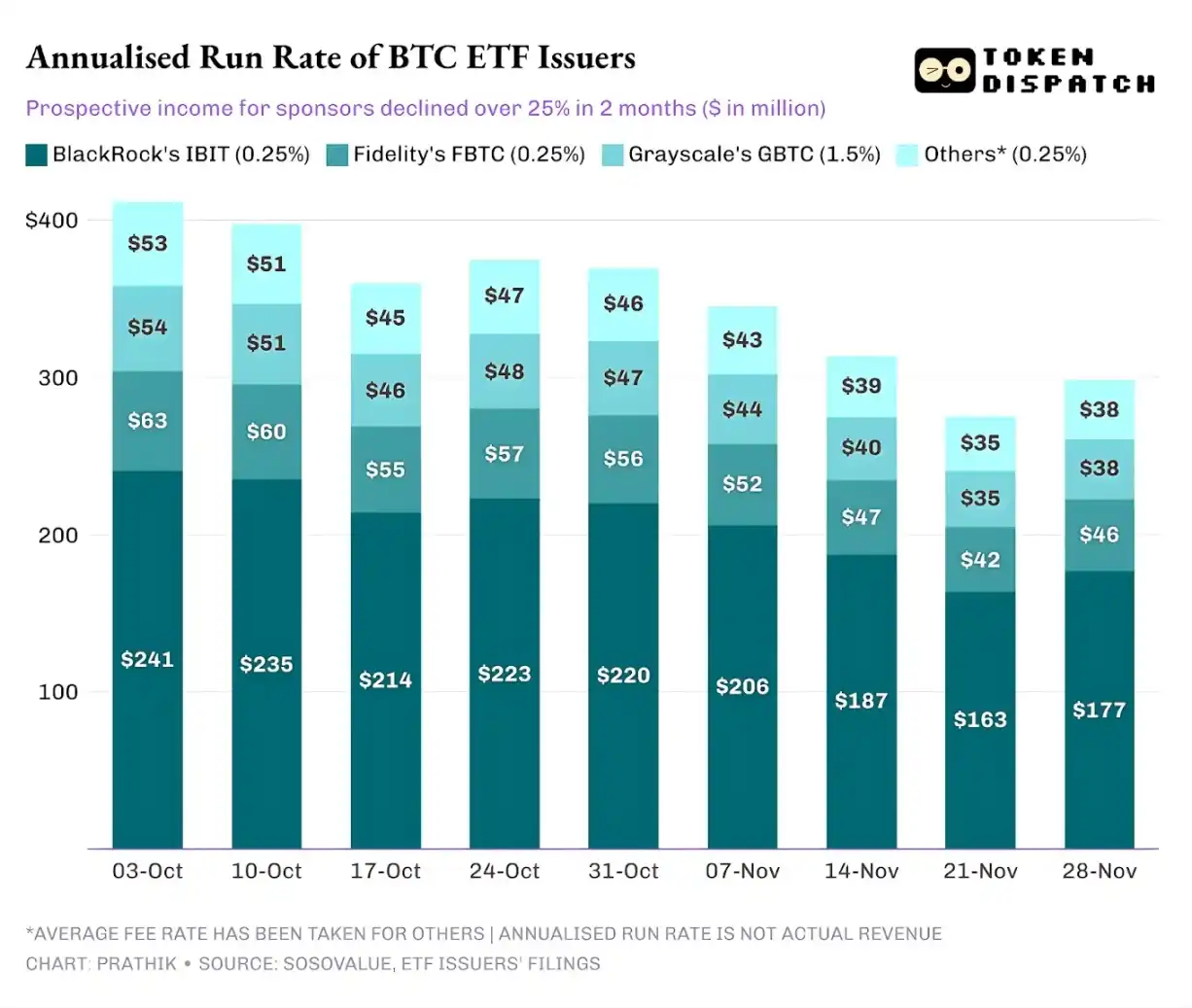

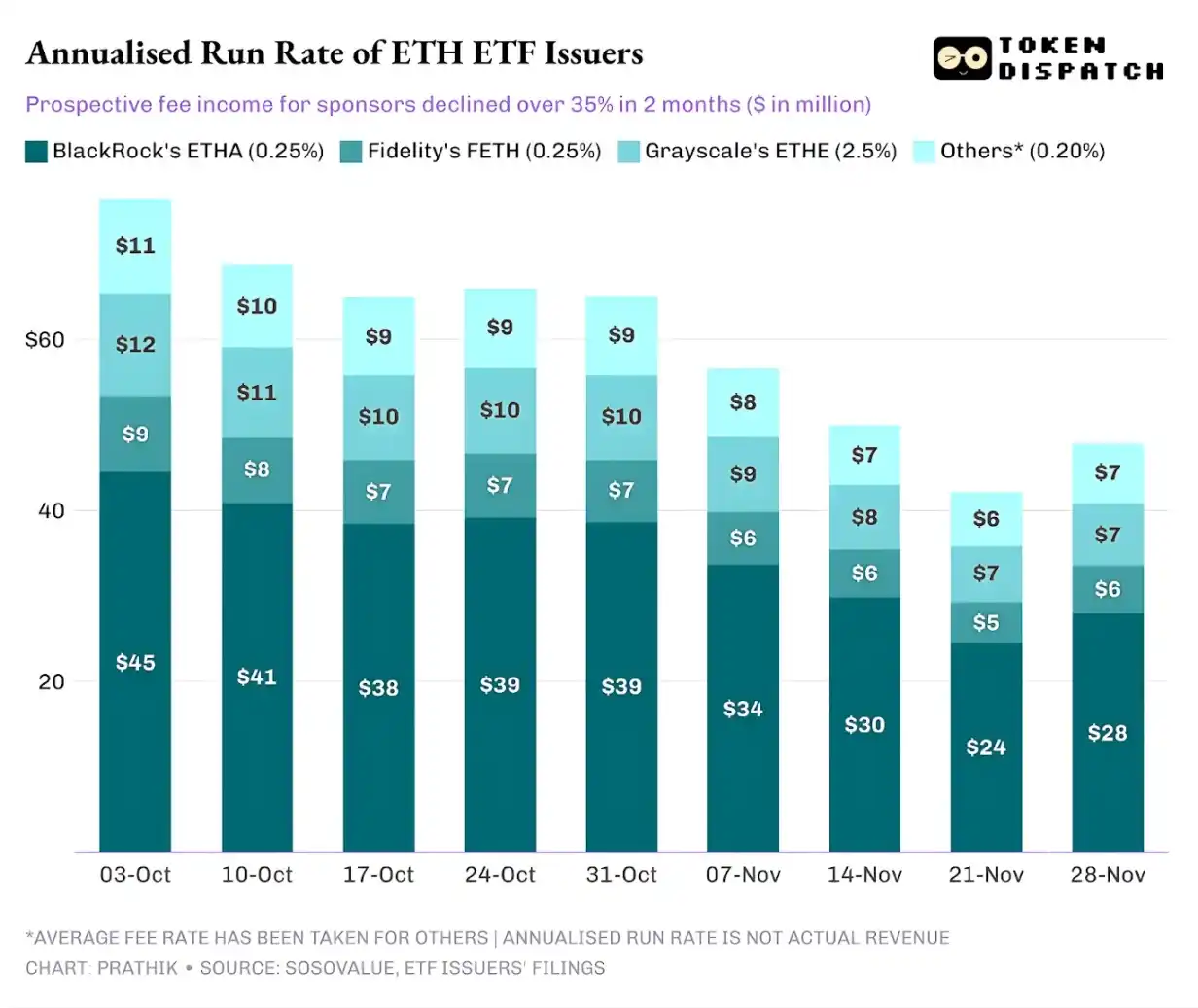

On October 3, the total assets managed by bitcoin and ethereum ETF issuers reached $195 billion. Combined with the above fee rates, the size of their fee pool was considerable. But by November 21, the remaining asset size of these products was only about $127 billion.

If annualized fee income is calculated based on weekend AUM, in the past two months, the potential income of bitcoin ETFs dropped by more than 25%; ethereum ETF issuers were even more affected, with annualized revenue falling by 35% over the past nine weeks.

The Larger the Scale, the Harder the Fall

From the perspective of individual issuers, the capital flow behind the scenes shows three slightly different trends.

For BlackRock, its business characteristics are a combination of "scale effect" and "cyclical fluctuations." Its IBIT and ETHA have become the default choices for mainstream investors to allocate bitcoin and ethereum through ETFs. This allows the world's largest asset management institution to charge a 0.25% fee based on a huge asset base, especially when AUM hit record highs in early October, resulting in very lucrative returns. But this also means that when large holders chose to reduce risk in November, IBIT and ETHA became the most direct targets for selling.

The data is telling: BlackRock's bitcoin and ethereum ETFs saw annualized fee income drop by 28% and 38% respectively, both exceeding the industry average declines of 25% and 35%.

Fidelity's situation is similar to BlackRock's, just on a smaller scale. Its FBTC and FETH funds also followed the pattern of "inflows first, outflows later," with October's market enthusiasm eventually replaced by November's outflows.

Grayscale's story is more about "historical legacy issues." Once upon a time, GBTC and ETHE were the only large-scale channels for many US investors to allocate bitcoin and ethereum through brokerage accounts. But as BlackRock, Fidelity, and other institutions took the lead in the market, Grayscale's monopoly position no longer exists. To make matters worse, the high fee structure of its early products has led to continued outflow pressure over the past two years.

The market performance in October and November also confirms this investor tendency: when the market is good, funds shift to products with lower fees; when the market weakens, holdings are cut across the board.

The fee rate of Grayscale's early crypto products is 6-10 times that of low-cost ETFs. Although high fees can boost revenue figures, high fee rates will continue to drive away investors, compressing the asset base from which fees are earned. The remaining funds are often constrained by frictional costs such as taxes, investment mandates, and operational processes, rather than active investor choice; and every outflow reminds the market: once a better option appears, more holders will abandon high-fee products.

These ETF data reveal several key characteristics of the current institutionalization process of cryptocurrencies.

The spot ETF market in October and November shows that the crypto ETF management business is as cyclical as the underlying asset market. When asset prices rise and market news is positive, inflows boost fee income; but once the macro environment changes, funds quickly retreat.

Although large issuers have built efficient "fee channels" on bitcoin and ethereum assets, the volatility in October and November proves that these channels are equally vulnerable to market cycles. For issuers, the core issue is how to retain assets during a new round of market shocks and avoid large fluctuations in fee income due to changes in macro trends.

Although issuers cannot prevent investors from redeeming shares during sell-offs, income-generating products can partially cushion downside risks.

Covered call option ETFs can provide investors with premium income (Note: A covered call option is an options investment strategy in which an investor, while holding the underlying asset, sells a corresponding number of call option contracts. By collecting premiums, this strategy aims to enhance portfolio returns or hedge some risks.), offsetting part of the price decline of the underlying asset; staking products are also a feasible direction. However, such products must first pass regulatory review before they can be officially launched to the market.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Mars Morning News | Ethereum Fusaka upgrade officially activated; ETH surpasses $3,200

The Ethereum Fusaka upgrade has been activated, enhancing L2 transaction capabilities and reducing fees; BlackRock predicts accelerated institutional adoption of cryptocurrencies; cryptocurrency ETF inflows have reached a 7-week high; Trump nominates crypto-friendly regulatory officials; Malaysia cracks down on illegal Bitcoin mining. Summary generated by Mars AI. The accuracy and completeness of this summary are still undergoing iterative updates.

Do you think stop-losses can save you? Taleb exposes the biggest misconception: all risks are packed into a single blow-up point.

Nassim Nicholas Taleb's latest paper, "Trading With a Stop," challenges traditional views on stop-loss orders, arguing that stop-losses do not reduce risk but instead compress and concentrate risk into fragile breaking points, altering market behavior patterns. Summary generated by Mars AI. The accuracy and completeness of this summary are still being iteratively improved by the Mars AI model.

Incubator MEETLabs today launched the large-scale 3D fishing blockchain game "DeFishing". As the first blockchain game on the GamingFi platform, it implements a dual-token P2E system with the IDOL token and the platform token GFT.

MEETLabs is an innovative lab focused on blockchain technology and the cryptocurrency sector, and also serves as the incubator for MEET48.

Electricity theft exceeds $1 billion, Malaysian bitcoin miners face severe crackdown

In Malaysia, the crackdown on illegal bitcoin mining gangs has turned into a game of cat and mouse.