Fed vs BOJ: December Global Market 'Scripted Drama', Will Bitcoin Crash First?

In November, the US Dollar Index fluctuated due to expectations surrounding Federal Reserve policies and the fundamentals of non-US currencies; in December, attention should be paid to the impact of the Federal Reserve's leadership transition, the Bank of Japan's interest rate hike, and seasonal factors on bitcoin and the US dollar. Summary generated by Mars AI. The accuracy and completeness of this content are still being iteratively improved.

I. November Review: Hawk-Dove Tug-of-War and the "Race to the Bottom" Among Non-US Currencies

In November, the US Dollar Index formed a double-top structure at the key resistance level of 100.3, displaying a typical M-shaped oscillation pattern.

Behind this movement were two main lines of intense contention: the repeated reversal of Federal Reserve policy expectations, and the intensifying divergence in the fundamentals of non-US currencies.

First, expectations for a Fed rate cut in December experienced roller-coaster-like fluctuations. At the beginning of November, Powell's hawkish remarks after the FOMC meeting temporarily suppressed the probability of a December rate cut, emphasizing that "a rate cut is not a foregone conclusion," which pushed the Dollar Index back to the 100 mark.

This phase of dollar strength stemmed from a repricing of the interest rate path—despite the Fed having already cut rates by 50 basis points in both September and October, Powell's concerns about inflation resilience, combined with a temporary rebound in non-farm payroll data, led the market to start trading on expectations of "higher for longer" rates.

However, the turning point came on November 6, when the US ADP private employment report unexpectedly weakened, revealing cracks in the labor market for the first time and rapidly heating up rate cut expectations. Subsequently, internal Fed officials sent mixed hawkish and dovish signals: dovish voices from Waller and Mester clashed with the cautious stance of Cook and others, causing the market to remain on the sidelines. It was not until November 21, when New York Fed President Williams released a dovish signal that "further rate cuts may come soon," that the probability of a December rate cut soared to over 70%, and the dollar fell in response.

Secondly, the "race to the bottom" logic among non-US currencies amplified dollar volatility. At the beginning of November, the pound sterling plunged 300 points in a single day due to concerns over fiscal sustainability, and the yen depreciated to the 157 level under government debt pressure. By the end of the month, the situation reversed: expectations of a Russia-Ukraine ceasefire boosted the euro, the UK budget temporarily eased debt panic, and rising expectations of a Bank of Japan rate hike collectively drove a rebound in non-US currencies.

This volatility highlights the passive nature of the Dollar Index—its movements are not entirely dictated by US fundamentals, but are a composite result of global risk appetite and monetary policy differentials.

II. Core Variables for December: The Ultimate Showdown of Three Forces

1. The Fed's "Politicization" Risk: The Hassett Effect and the Probability of a Rate Cut

The primary uncertainty facing the dollar in December comes from the change in Fed chairmanship. Trump has made it clear that he "has someone in mind," with White House National Economic Council Director Hassett emerging as the top favorite. His dovish stance is extremely pronounced, publicly stating that if he were to lead the Fed, he would "cut rates immediately."

If the nomination is announced in advance, the market may preemptively trade on the logic of "politically driven easing," putting short-term pressure on the dollar.

However, the December FOMC meeting itself remains crucial. The current 90% probability of a rate cut priced in by the futures market is not set in stone—if November non-farm payrolls exceed expectations or inflation rebounds, the Fed may once again deliver a "hawkish rate cut," i.e., cut rates by 25 basis points but signal a pause. In this scenario, the dollar may rebound on the logic of "sell the rumor, buy the fact."

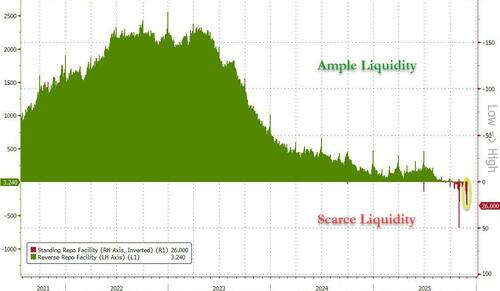

In addition, the Fed will end its balance sheet reduction on December 1, and the marginal improvement in liquidity may partially offset the downward pressure on the dollar from a rate cut.

2. The Bank of Japan's "Historic Shift": How Rate Hike Expectations Reshape the FX Landscape

The Bank of Japan's policy meeting on December 19 could become a watershed moment in the global liquidity cycle.

Governor Kazuo Ueda made it clear on December 1 that "the pros and cons of a rate hike will be weighed at the next meeting," and that persistently core inflation above 2% would be the basis for a policy adjustment. The market's probability for a December rate hike has soared from 30% two weeks ago to 80%, and this repricing has directly triggered a short squeeze in the yen, pushing USD/JPY below the 155 mark. If the Bank of Japan raises rates as expected, it will break a decade-long negative interest rate policy and could trigger a large-scale unwinding of carry trades.

In the short term, USD/JPY may fall back to the 153-155 range; in the medium to long term, this signals the end of the global "cheap yen" era, intensifying the pressure for funds to flow back from US Treasuries and other dollar assets to Japan. However, beware of a "sell the news" scenario—similar to the short-term pullback in the yen after the March 2024 rate hike, carry trades may regroup once policy becomes clear.

3. Seasonality and Structural Contradictions: The Dollar's Long-Term Weakness Is Hard to Reverse

Historical data shows that over the past 10 years, the probability of the Dollar Index falling in December is as high as 80% (rising only in 2016 and 2024). This pattern is due to seasonal factors such as the end of year repatriation of overseas corporate profits and active global asset rebalancing trades. In December 2025, this pattern may be reinforced by the following factors:

- Liquidity improvement: The Fed ending balance sheet reduction and potential rate cuts jointly increase dollar supply;

- Fiscal pressure: The US deficit ratio surpasses 5%, and the "Big and Beautiful" bill may exacerbate debt concerns;

- De-dollarization trend: Diversification of foreign exchange reserves in many countries continues to weaken dollar demand.

However, economic weakness in the eurozone (zero growth in Germany in Q3) and geopolitical risks may provide temporary support for the dollar, so beware of repeated market swings.

III. Bitcoin December Outlook: The "Reverse Thermometer" of Liquidity Expectations

The negative correlation between Bitcoin and the Dollar Index is particularly pronounced in 2025.

When expectations for dollar liquidity easing rose in early October, Bitcoin soared to a historic high of $126,000; after the dollar index rebounded in November, Bitcoin plummeted 30% to $82,000. This linkage stems from Bitcoin's nature as a "global liquidity-sensitive asset"—its price is highly sensitive to dollar interest rate expectations.

Historically, Bitcoin tends to perform poorly in December: in the past 13 years, it has only risen 5 times, with the largest declines occurring in 2013 (-34%) and 2021 (-19%).

This pattern mirrors the seasonal strength of the Dollar Index.

In December 2025, Bitcoin may face a tug-of-war between bulls and bears:

- Bullish factors: If the Fed delivers a rate cut or the Bank of Japan's rate hike triggers a collapse in carry trades, improved global liquidity expectations will boost Bitcoin;

- Bearish risks: If the Fed stands pat or US inflation data exceeds expectations, tighter dollar liquidity will suppress Bitcoin.

The key threshold is at $88,000-$90,000—if Bitcoin fails to effectively reclaim this level, it may further test the previous low of $75,000; conversely, if the Dollar Index weakens due to seasonality or a shift by non-US central banks, Bitcoin may resume its upward trend.

It should be noted that Bitcoin's recent volatility has increased significantly, with a long-short ratio imbalance (November's long liquidations were 2.3 times those of shorts), highlighting the fragility of market sentiment.

IV. Epilogue: The Prelude to the Currency War and Asset Rotation at the End of 2025

The global market in December is akin to a stress test of faith in the fiat currency system. Whether the dollar can break the "December decline" curse depends on whether the Fed or the Bank of Japan pulls the trigger on a policy shift first; while Bitcoin's sharp volatility serves as a litmus test for the abundance of global liquidity. As Trump's tariff policies become entangled with the Fed's political independence, and Japanese bond yields break new highs since 2008, the market has shifted from simple economic data trading to a re-pricing of monetary sovereignty and credit.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Musk calls Bitcoin an energy-based "physics currency"

Bitcoin battles $50K price target as Fed adds $13.5B overnight liquidity

Bitcoin valuation metric projects 96% chance of BTC price recovery in 2026