The Eve of Bitcoin's Year-End Surge: ETF Drains Liquidity, Rate Cuts Ignite the Market, and the Blueprint for Altcoins to Double Is Already Written

The cryptocurrency market showed signs of recovery in October 2025, with investor sentiment shifting from cautious to cautiously optimistic. Net capital inflow turned positive, institutional participation increased, and the regulatory environment improved. Bitcoin spot ETF saw significant capital inflows, while the approval of altcoin ETFs injected new liquidity into the market. On the macro level, expectations of a Federal Reserve rate cut intensified, and the global policy environment became more favorable. Summary generated by Mars AI. The accuracy and completeness of this summary are still being improved and updated.

Overall Market Situation: Transition from Caution to Cautious Optimism

Entering late October 2025, after a period of adjustment, the cryptocurrency market is showing clear signs of recovery. The prevailing cautious sentiment that dominated the market over the past two months is gradually dissipating, especially after the sharp correction on October 11. Investor sentiment has shifted from panic to a more rational stance. Multiple key indicators suggest that the market bottom has been effectively tested, and new bullish momentum is building.

The market recovery is not only reflected in price levels but is more profoundly seen in capital flows, institutional participation, and multidimensional improvements in the regulatory environment. Since late October, net capital inflows have turned positive, batches of altcoin ETFs have been approved, and expectations for global monetary easing are rising. These factors together have injected new vitality into the market.

As of October 29, data shows that the total cryptocurrency market capitalization has rebounded to $3.97 trillion, up 2.06% from last week. The market fear index has also recovered from its lows to 39, indicating that while investor sentiment remains cautious, it has clearly improved.

Positive changes in market structure are also evident in the completion of the deleveraging process. The crash on October 11 liquidated a large number of high-leverage positions. In the four weeks leading up to October 22, the total amount of liquidations across the network gradually declined, and excessive speculation in the derivatives market has been effectively curbed. Currently, bitcoin contract open interest has returned to healthy levels, funding rates remain positive but not overheated, indicating a more solid market foundation.

ETF Market: The Core Channel for Large-Scale Institutional Capital Inflows

Bitcoin Spot ETF: The Core Barometer of Institutional Allocation Demand

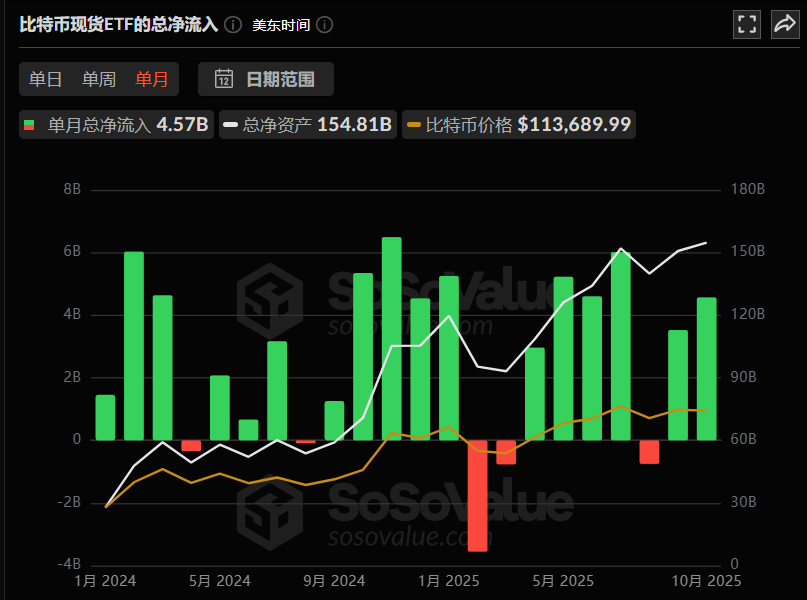

The most prominent highlight in the cryptocurrency market in October was concentrated in the ETF sector, where capital flows and institutional behavior jointly confirmed the return of market confidence. Bitcoin spot ETFs saw a cumulative net inflow of $4.57 billion this month.

As of October 29, the total assets under management of bitcoin spot ETFs have climbed to a historic high of $154.8 billion, accounting for 6.8% of bitcoin’s total market capitalization, making it an important reservoir of market capital.

Looking at weekly data, the net inflow for the week of October 20-27 reached $446 million, with BlackRock’s IBIT fund standing out by absorbing $324 million in a single week. Its current holdings have surpassed 800,000 BTC. This data highlights the strong bullish stance of leading financial institutions on bitcoin.

For traditional financial markets, ETF capital inflows are a core indicator reflecting market expectations—compared to the subjectivity of social media hype and the technical limitations of candlestick charts, ETF capital flows more objectively reflect the real allocation intentions of institutions and long-term funds.

Institutional Allocation Behavior: Crypto Assets Become an Important Part of Investment Portfolios

A significant feature of this market rally is the “strengthening of institutional attributes.”

Leading financial institutions continue to increase their crypto asset allocations: Morgan Stanley has opened bitcoin and ethereum allocation channels to all wealth management clients; JPMorgan now allows institutional clients to use bitcoin as loan collateral, further enriching the application scenarios for crypto assets.

Latest data shows that the average institutional allocation to crypto assets has risen to 19%, a record high; and 85% of institutions say they have completed or plan to start crypto asset allocation in the short term.

This indicates that crypto assets are gradually becoming a standardized component of institutional investment portfolios, rather than marginalized speculative assets.

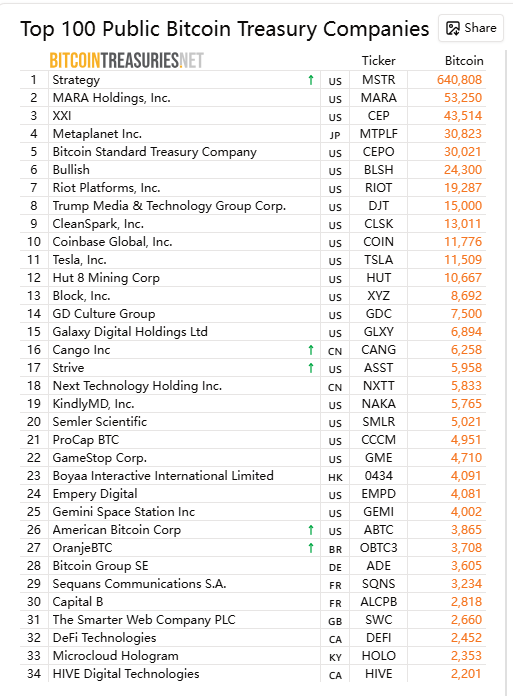

In terms of corporate capital allocation, traditional financial entities such as Block, Inc. have included cryptocurrencies on their balance sheets, with reserves exceeding 8,000 bitcoins, worth about $550 million, demonstrating long-term value recognition.

Ethereum ETF and Capital Rotation: Strategic Adjustments Behind Short-Term Outflows

In contrast to the strong performance of bitcoin spot ETFs, ethereum ETFs showed relative weakness in October, with a cumulative net inflow of $930 million.

From a market logic perspective, this phenomenon can be interpreted as a “capital rotation signal”: on one hand, some funds are shifting from ethereum to bitcoin and solana, which have clearer short-term upside potential;

On the other hand, it may also be that institutions are reallocating funds in preparation for new types of ETF products (such as ethereum futures ETFs and altcoin ETFs), laying the groundwork for a new round of allocations.

This rotation phenomenon is not uncommon in history; a similar situation occurred at the beginning of 2024, after which ethereum saw significant capital inflows following the Cancun upgrade.

Altcoin ETFs: Batch Approvals Open a New Liquidity Channel

On October 28, the U.S. market welcomed the first batch of altcoin ETFs, covering three mainstream altcoin projects: Solana, Litecoin, and Hedera. Specifically, these include the SOL ETF launched by Bitwise and Grayscale, as well as the LTC ETF and HBAR ETF approved for trading on Nasdaq by Canary Capital.

This development marks further recognition of the crypto asset class by the traditional financial system. Notably, the first batch of altcoin ETFs is only the prelude to the market.

According to public data, there are currently 155 altcoin ETFs pending approval, covering 35 mainstream altcoin assets. The market expects their initial capital inflows to exceed the combined initial inflows of the first two rounds of bitcoin and ethereum ETFs. If all these ETFs are approved, they will bring an unprecedented “liquidity shockwave” to the crypto market.

Historically, the launch of bitcoin ETFs attracted over $50 billion in cumulative capital, while ethereum ETFs brought an additional $25 billion in assets.

Essentially, ETFs are not just financial products but also “standardized channels” for capital to enter the crypto market—when the channel expands from bitcoin and ethereum to SOL, XRP, LINK, AVAX, and other altcoins, the entire crypto market’s valuation system will be restructured, and the liquidity and pricing efficiency of small and mid-cap coins are expected to improve significantly.

Institutional layouts in the altcoin ETF sector are deepening: ProShares plans to launch the CoinDesk 20 ETF, which will track the performance of 20 crypto assets including BTC, ETH, SOL, and XRP; REX-Osprey has launched a 21-Asset ETF, innovatively allowing holders to earn staking yields from tokens such as ADA, AVAX, NEAR, SEI, and TAO, further enriching ETF product yield models. For Solana alone, there are currently 23 ETFs awaiting approval. This intensive layout clearly indicates that institutions’ risk appetite for crypto assets is gradually increasing, with the risk curve extending from bitcoin to the entire DeFi ecosystem.

Macro Environment: Dual Drivers of Liquidity Easing Expectations and Policy Friendliness

Federal Reserve Monetary Policy: Rate Cut Expectations Open Up Liquidity Space

Aside from ETF factors, macro-level expectations of liquidity easing are another core variable driving the market.

On October 29, market data showed a 98.3% probability that the Federal Reserve would cut rates by 25 basis points, and this expectation has already been reflected in market trends—the US dollar index weakened, risk assets collectively rose, and bitcoin prices broke through the $114,900 mark. From a capital logic perspective, rate cuts mean lower overall funding costs, and excess funds need to seek higher-yielding outlets.

In 2025, with traditional markets (such as stocks and bonds) lacking clear growth highlights, the crypto market, which still has “narrative space,” has become the focus of capital attention, attracting funds from traditional markets to migrate into crypto.

US core CPI data for September also supports expectations of a rate cut.

The core CPI for September recorded a month-on-month rate of 0.2%, below the expected 0.3%, with inflationary pressures continuing to ease. With the government shutdown ongoing and the job market cooling, a Fed rate cut in October has become highly probable. According to the latest CME “FedWatch” data, the probability of a 25 basis point rate cut in October is as high as 96.7%, and the probability of a cumulative 50 basis point cut by December is 94.8%.

Global Debt Cycle and Liquidity Creation

According to Raoul Pal’s global debt cycle analysis, the current total global debt has reached about $300 trillion, with about $10 trillion in debt (mainly US Treasuries and corporate bonds) coming due soon, requiring massive liquidity injections to prevent a spike in debt yields. Raoul Pal estimates that every $1 trillion increase in liquidity will drive a 5-10% return in risk assets such as stocks and cryptocurrencies;

For the crypto market, during the $10 trillion debt refinancing process, it is expected that $2-3 trillion will flow into risk assets, potentially pushing BTC from its 2024 low of $60,000 to over $200,000 by 2026. This relationship between the debt cycle and liquidity creation essentially reconstructs the operating logic of the crypto market. The traditional four-year halving cycle may give way to a broader global liquidity cycle, further strengthening the linkage between the crypto market and traditional financial markets.

Policy Environment: Regulatory Shift to Friendliness, Accelerated Compliance Process

This round of market bullishness is not only driven by capital but also supported by policy.

On October 27, the White House nominated former crypto lawyer Michael Selig as Chairman of the US Commodity Futures Trading Commission (CFTC). His previous friendly stance toward the crypto industry has injected confidence into the market. At the same time, the US Securities and Exchange Commission (SEC) updated the creation mechanism for exchange-traded products (ETPs), allowing crypto ETFs to conduct “in-kind redemptions,” greatly simplifying ETF operations and lowering the threshold for institutional participation.

Currently, the US regulatory attitude toward the crypto market has shifted from “suppression” to “guiding compliance.” The government no longer simply restricts crypto innovation but is improving the regulatory framework to promote the development of the crypto industry within a compliant structure, laying the foundation for the market’s long-term healthy operation.

In addition, Trump’s pardon of Binance founder Changpeng Zhao (CZ) is also seen as an important signal of improvement in the US crypto regulatory environment.

Globally, regulatory frameworks are also becoming clearer. Kenya has passed the “2025 Virtual Asset Service Providers Act,” establishing a dual regulatory system of “central bank + capital markets authority”; the implementation of the European MiCA framework and the launch of dual-currency ETFs in Hong Kong have made the global regulatory environment clearer and reduced compliance uncertainty.

Geopolitical Factors: Easing China-US Trade Relations Boost Risk Assets

On October 25-26, China and US economic and trade teams held a new round of consultations in Kuala Lumpur, reaching preliminary consensus on several important economic and trade issues. The easing of China-US trade tensions has significantly boosted global risk appetite. As a result, spot gold and silver opened lower, oil prices strengthened, and US stock futures rose across the board. As a key representative of risk assets, the crypto market has also benefited from the improved macro environment. This breakthrough means that trade frictions between the world’s two largest economies have eased, creating a more favorable environment for global capital flows. As a highly globalized asset class, the crypto market naturally benefits from this.

Reconstructing Market Cycle Theory: From Halving Narrative to Liquidity Narrative

Arthur Hayes: The Four-Year Cycle Is Dead, the Liquidity Cycle Lives Forever

In a blog post titled “Long Live the King” published in late October, former BitMEX CEO Arthur Hayes challenged the traditional cycle theory of the crypto market. He argues that although some traders expect bitcoin to soon reach a cycle peak and crash in 2026, the current market logic has fundamentally changed—the “four-year halving cycle” for bitcoin is no longer valid, and the real core variable driving market trends is the “global liquidity cycle,” especially the resonance of US dollar and RMB monetary policies.

Hayes points out that the past three crypto bull and bear cycles (2009-2013, 2013-2017, 2017-2021) appeared to follow the “post-halving bull market, four-year cycle” pattern, but in essence, each cycle coincided with a “credit expansion cycle” of the US dollar or RMB: 2009-2013, the Federal Reserve launched unlimited quantitative easing (QE), and China simultaneously started large-scale credit issuance; 2013-2017, RMB credit expansion fueled the ICO boom, injecting liquidity into the crypto market; 2017-2021, the Trump and Biden administrations successively launched “helicopter money” policies, resulting in a global liquidity glut. When the pace of credit expansion in the US dollar or RMB slowed, the bitcoin bull market also ended—in essence, bitcoin is a “barometer” of global monetary easing, not independently driven by halving events. Entering 2025, the “halving-driven” logic has completely collapsed: the monetary policies of the US and China have entered a “new normal of sustained easing,” with political pressure requiring monetary and fiscal policies to remain loose, and liquidity no longer tightening according to traditional cycles. The US needs to “heat up the economy” to dilute high debt levels, with the Trump administration continuing to pressure the Fed to cut rates and expand fiscal spending; China, facing deflationary pressure, is also gradually expanding credit, with both countries continuously injecting funds into the market. Based on this, Hayes concludes: “The four-year cycle is dead; the real cycle is the liquidity cycle. As long as the US and China continue to maintain monetary easing, bitcoin will remain on an upward trend.” This means that the future trend of the crypto market will no longer be constrained by the “halving timetable,” but will depend on the direction of US dollar and RMB monetary policies. He ends with “The king is dead, long live the king,” metaphorically marking the end of the traditional halving cycle and the official start of a new liquidity-driven cycle.

Raoul Pal: The 5.4-Year Cycle Theory Reconstructs the Traditional Cycle Model

Former Goldman Sachs executive and Real Vision founder Raoul Pal’s “5.4-year cycle theory” fundamentally reconstructs the traditional four-year bitcoin halving cycle. He believes that the traditional four-year cycle is not driven by the bitcoin protocol itself (halving events), but is the result of the past three cycles (2009-2013, 2013-2017, 2017-2021) coincidentally aligning with the “global debt refinancing cycle,” with each cycle ending due to monetary tightening rather than halving events. The core trigger for this theoretical shift is the structural change in the US debt structure in 2021-2022: in a near-zero interest rate environment, the US Treasury extended the average weighted maturity of its debt from about four years to 5.4 years. This adjustment not only changed the US debt refinancing timetable but, more importantly, reshaped the global liquidity release rhythm, pushing bitcoin’s cyclical peak from the traditionally expected Q4 2025 to Q2 2026, and indicating that Q4 2025 will be a key window for market recovery. From a data perspective, Raoul Pal’s model further predicts that Q2 2026 will see a historic peak in global liquidity; when the US ISM Manufacturing Index breaks above 60, bitcoin will enter a rapid growth “banana zone,” with a target price range of $200,000 to $450,000. This prediction, based on in-depth research into the relationship between debt cycles and asset prices, provides a new perspective for understanding market trends.

Conclusion

The crypto market in October 2025 is at a critical turning point. The traditional halving cycle theory is giving way to the global liquidity cycle narrative, institutional capital is pouring in on a large scale through standardized channels such as ETFs, the regulatory environment remains friendly, and on-chain data confirms increased market activity. These factors together are driving the market into a new stage. Unlike previous cycles, the driving forces of this market are more diversified, institutionalized, and fundamentally based.

The trend of the market shifting from a “marginal speculative asset” to a “mainstream allocation asset” is clear, and the valuation system is being reconstructed. Although short-term volatility is inevitable, the medium- to long-term outlook for the crypto market remains optimistic against the backdrop of global liquidity easing, increased institutional participation, and continuous technological innovation. Investors need to recognize changes in market structure, understand market operating logic from a more macro perspective, and maintain risk awareness in order to seize opportunities and achieve investment goals amid change. As the crypto market further integrates into the global financial system, its linkage with traditional financial markets will be further strengthened, requiring investors to have a more comprehensive analytical framework and more professional investment strategies.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitwise Clients Buy $69.5M in Solana

Quick Take Summary is AI generated, newsroom reviewed. Bitwise clients bought $69.5 million in Solana, signaling strong institutional confidence. Solana institutional demand continues to rise amid increasing DeFi and Web3 adoption. The Bitwise Solana investment strengthens the firm’s role in institutional crypto expansion. Growing Solana price momentum suggests sustained investor interest and market optimism.References JUST IN: Bitwise clients buy $69.5 million worth of $SOL.

TWINT wants to open platform for stablecoins and tokenized deposits

Regulated crypto yield wins as institutions demand substance

Four XRP price charts that are predicting a rally toward $3