Has SOL Bottomed Out? Multi-dimensional Data Reveals the True Picture of Solana

Despite new chains like Sui, Aptos, and Sei making continuous efforts, they have not posed a substantial threat to Solana. Even though some traffic has been diverted by application-specific chains, Solana firmly maintains its leading position among general-purpose blockchains.

Author: @blocmates

Translation: Odaily

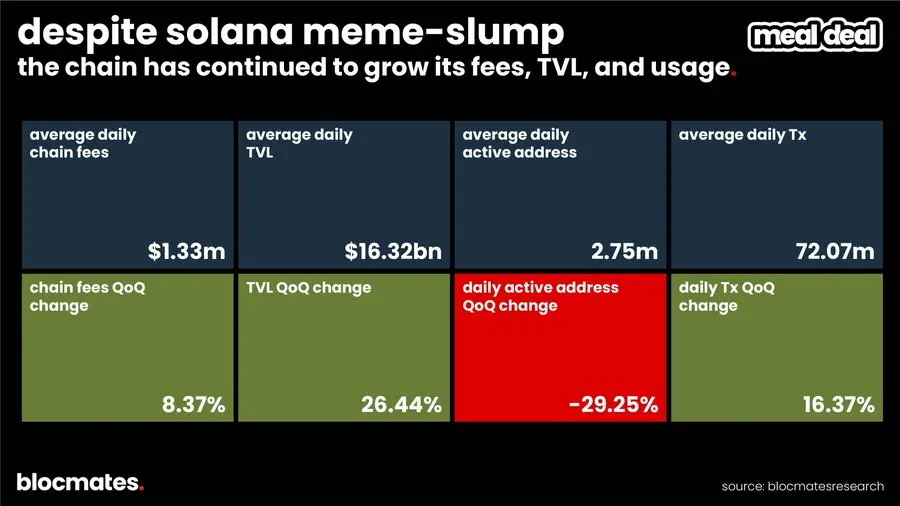

Q3 2025 was a “tale of two sides on the same chain” for Solana. On the surface, the “meme tide” receded, bringing a clear cooling effect: daily active addresses declined, and user dominance was gradually eroded by competitors. However, beneath the surface, the fundamentals of this chain have become increasingly solid. The Solana core team has maintained a high frequency of iterations, continuously advancing one of the most ambitious technical roadmaps in the crypto industry; meanwhile, its TVL grew by over 26% in Q3, and stablecoin supply has nearly tripled since the beginning of the year.

This report systematically reviews the core technical upgrades (such as Alpenglow and Agave) that are defining Solana’s future, provides an in-depth analysis of on-chain data performance and the health of ecosystem applications, and summarizes our key views on how Solana can consolidate its status as the “default high-performance public chain.”

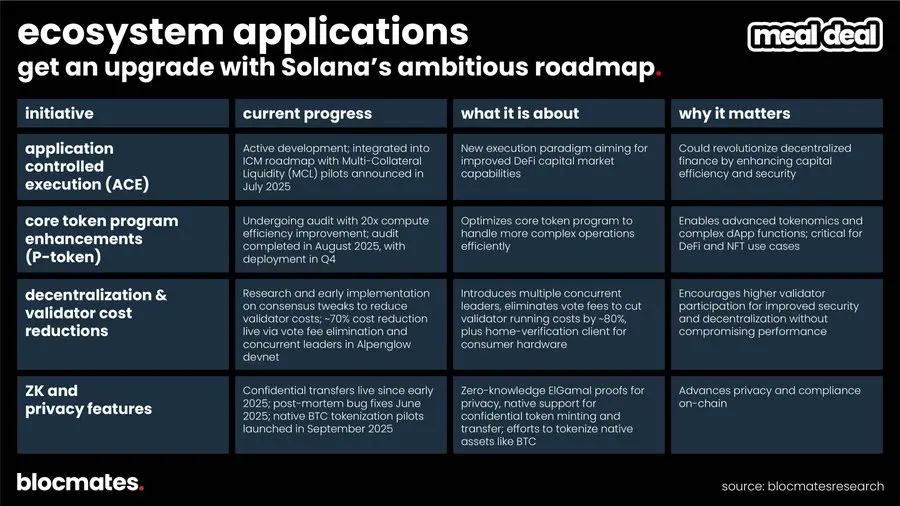

Multi-pronged Technological Innovation

While most users on the platform are busy chasing the latest meme trends, the @solana core team has been pushing forward an ambitious set of system-level upgrades. This is not about patching a single metric, but a comprehensive engineering effort to improve network performance, security, decentralization, and user experience. These upgrades can be roughly divided into three categories.

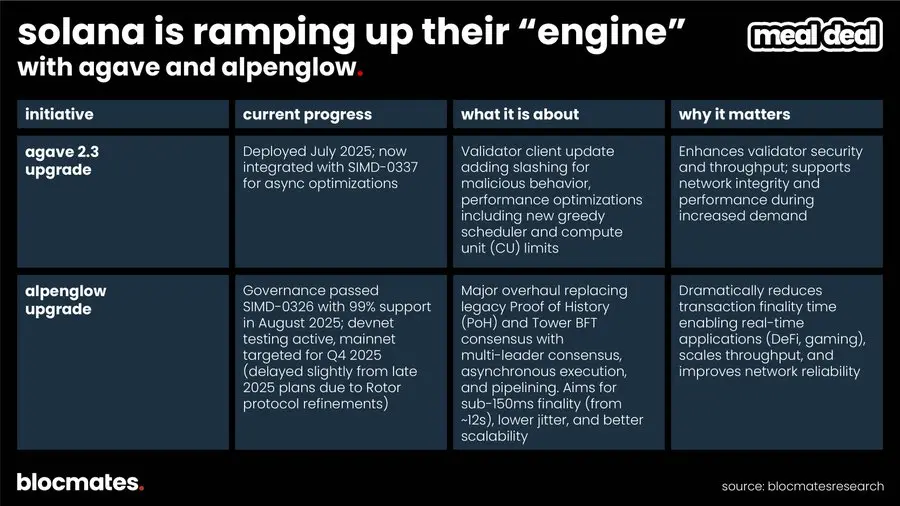

Category One: Core Engine (Consensus and Client)

This is a fundamental overhaul of Solana’s “engine,” aiming to improve performance, speed, and security from the most basic level. There is a great visual chart available if you’re curious about the current staking ecosystem.

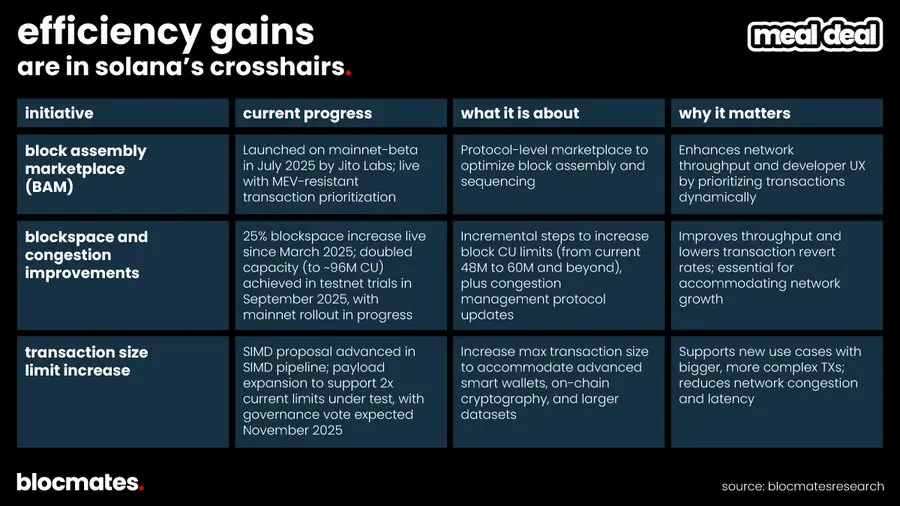

Category Two: Network Highway (Throughput and Efficiency)

This part of the work focuses on widening the network “lanes” and optimizing traffic scheduling after improving the underlying performance, so that the network can handle higher future loads without congestion. If institutional users are to truly come on-chain in the future, low latency and a stable experience are foundational, not optional.

Category Three: Destination (New Capabilities at the Ecosystem and Application Layer)

This category of upgrades is aimed directly at developers and end users, designed to provide more new features, support new types of applications, and further enhance the chain’s level of decentralization. In other words, this is the module that allows the “chain to do more.”

Practical Impact of Technical Improvements

From a practical usage perspective:

- Alpenglow: Final confirmation speed below 150ms (UTC+8) allows retail users to use high-frequency DeFi, gaming, or micropayment applications on-chain, with performance approaching Binance’s 100ms (UTC+8) and Aptos’s 200ms (UTC+8).

- Firedancer: Potential capacity of over 1 million TPS far exceeds Ethereum and its L2s (such as OP’s ~2k TPS), Sui’s 300k TPS, and centralized exchanges (Coinbase peak ~500k TPS). It also significantly reduces systemic risk from single client failures (Ethereum’s Geth still accounts for 60% of nodes).

- Block space improvements, congestion relief, and transaction size optimization: Enhance the overall experience of using the chain, enabling finer-grained microtransactions and rapid transactions, while reducing failures due to congestion.

- Decentralization and lower node costs: Lower technical barriers allow more users to run nodes, improving the network’s security and decentralization.

- ZK and privacy support: Provide a compliant, private, and secure foundation for RWA and institutional users to enter.

- BAM (Fair Trading, MEV Resistance): Ensure transaction fairness and protect users from MEV losses, making the on-chain experience closer to the predictable, low-cost environment of a CLOB.

- ACE (Multi-collateral Liquidity): Further deepen DeFi capital markets, enabling competition with platforms like Aave and supporting more complex financial instruments.

Validation Through On-chain Stress Testing

In July 2025, Pump.fun’s event became a real “stress test” of Solana’s performance. @pumpfun raised $500 million and $100 million through on-chain and centralized exchanges, respectively, within just 12 minutes (UTC+8), corresponding to a valuation as high as $4 billion. During this period, 3,878 investors transparently completed subscriptions on Solana’s Raydium, Jupiter, and other DEXs, while some CEXs (such as Bybit) experienced lags due to multiple API failures, and about 2,500 confirmed investors were unable to place orders in time due to API delays and had to be refunded.

Does this mean we are witnessing a possible future—where decentralized blockchains begin to outperform centralized exchanges?

So Where Does Solana Stand Now? The Truth Revealed by Data

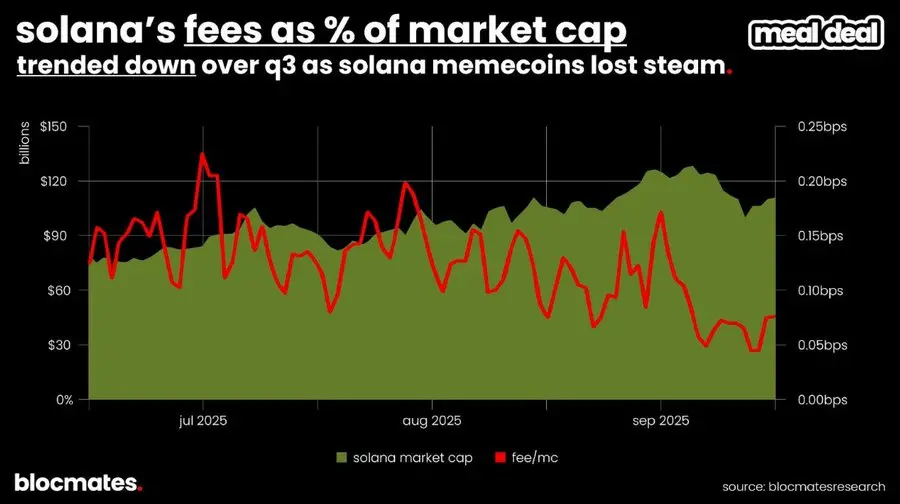

According to the data, as traders shifted from meme speculation to perpetual contracts, Solana’s on-chain revenue metrics were clearly affected: the ratio of on-chain fees to SOL market cap has dropped by more than 60% since the July peak.

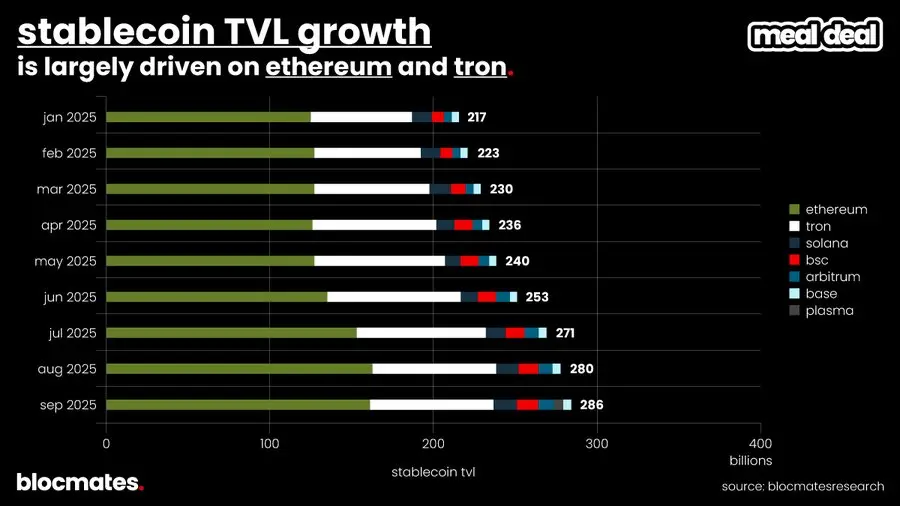

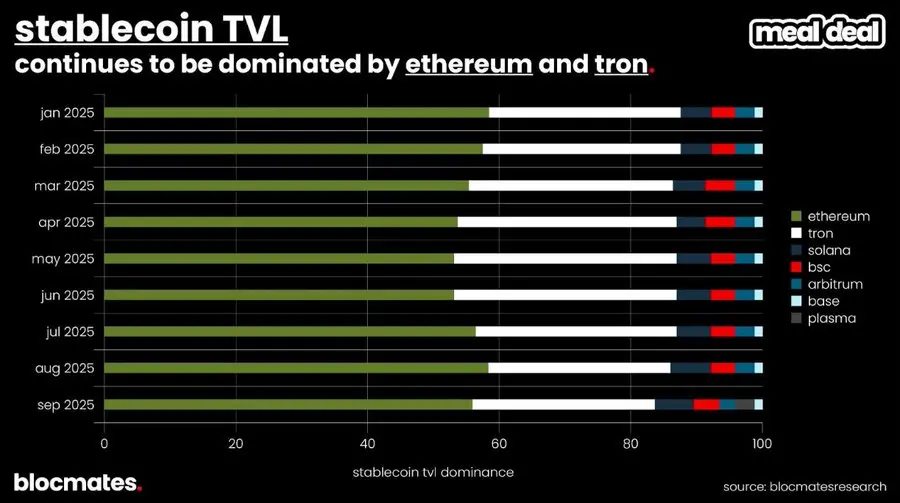

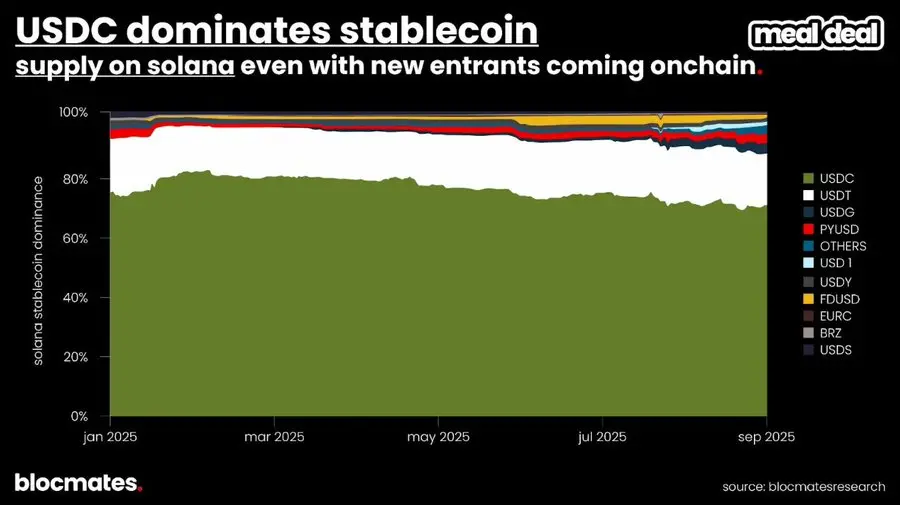

Meanwhile, despite ongoing discussions about stablecoins on Capitol Hill and Wall Street, the dominant players remain Ethereum and Tron, while Solana, Base, BSC, Arbitrum, and other chains are in the “second tier.”

Breaking down the stablecoin TVL share further, Ethereum and Tron have remained dominant over the past few quarters, while some emerging application chains—such as @Plasma —are gradually entering the picture.

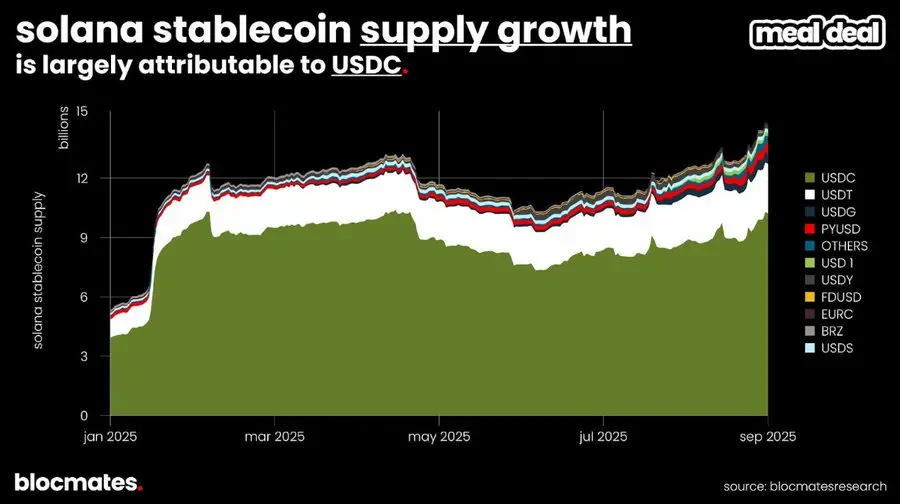

Nevertheless, Solana still provides a fast, low-cost, and highly liquid environment for USDC usage, which may be why Western Union chose to build its stablecoin business on Solana.

“Experimentation” will be one of the core themes of this report, and this spirit is also reflected in the stablecoin ecosystem: new projects are gradually eroding USDC’s dominance, bringing more competition to Solana’s stablecoin landscape.

Which Ecosystem Participants Are Driving Chain Growth?

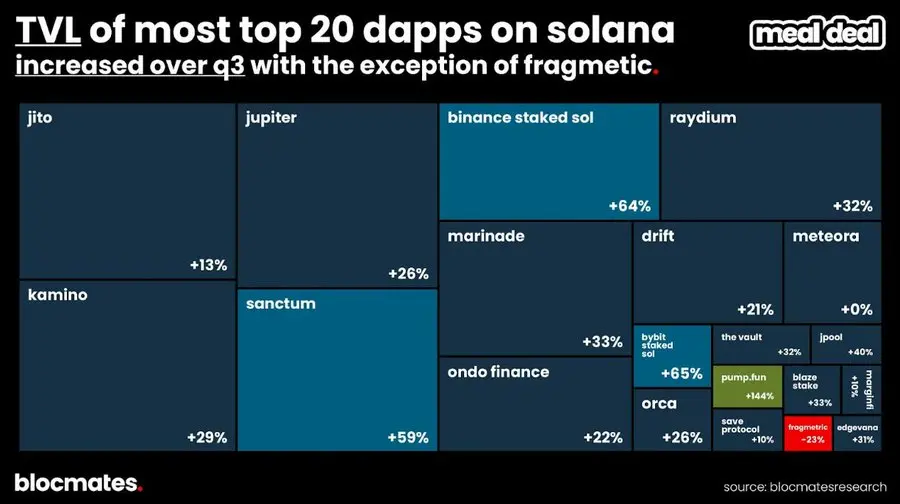

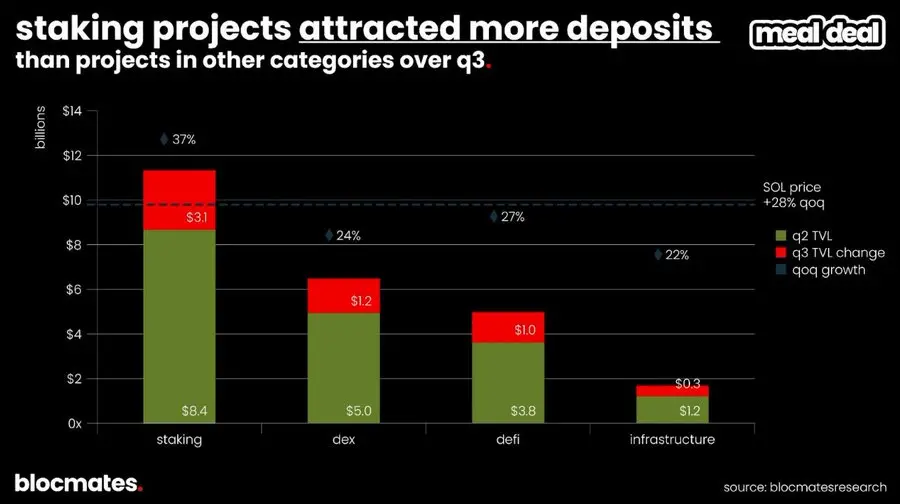

In terms of TVL growth, staking products were the absolute highlight among Solana applications in Q3, with staking SOL offered by Binance and Bybit, as well as products from @Sanctumso, all recording over 50% growth in Q3.

In contrast, DEX, DeFi, and infrastructure products also saw TVL increases, but none surpassed SOL’s own 28% rise—meaning when denominated in SOL, these categories actually saw net outflows over the past quarter.

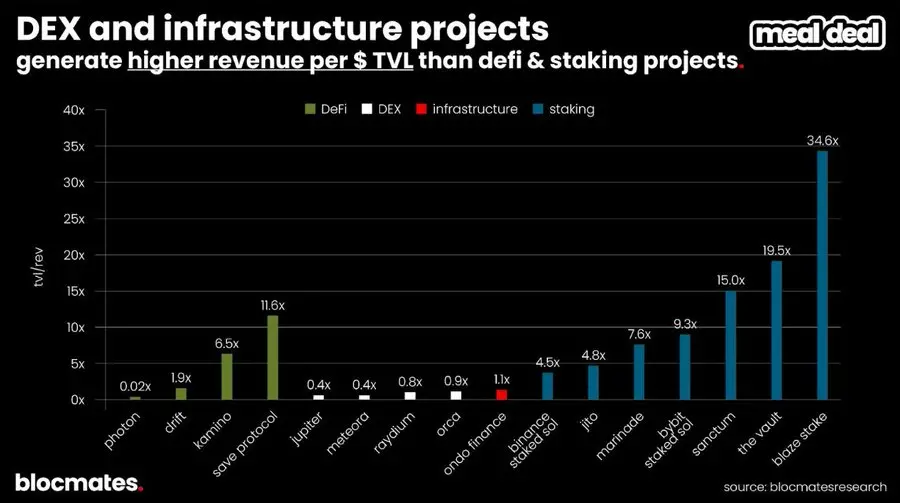

The shortcoming of staking products is their relatively weak profitability: on average, a staking protocol needs 21.7 times the TVL to reach the average revenue level of DEXs in this sample. This again illustrates a fact—in the crypto world, speculators contribute far more profit than savers.

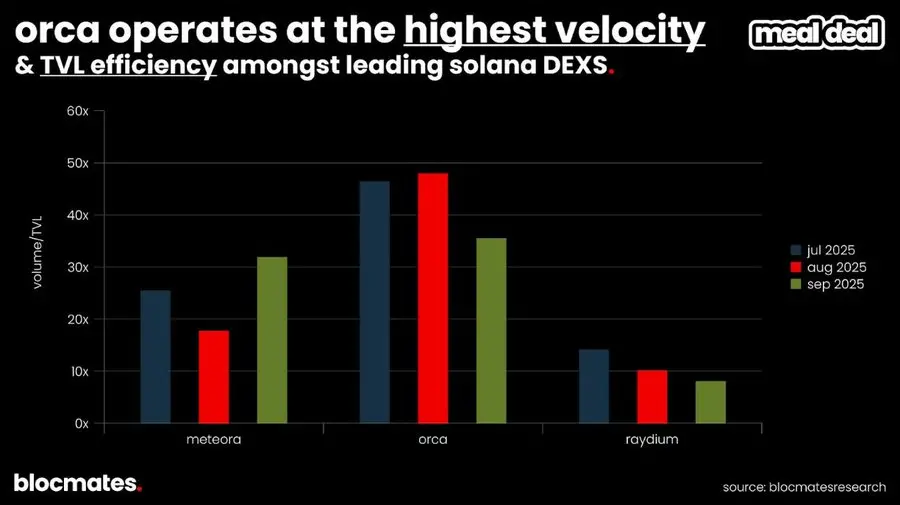

In the DEX sector, @Orca_so has consistently maintained a leading position in TVL efficiency (i.e., “trading speed”). For a given liquidity size, each dollar on Orca is traded most frequently.

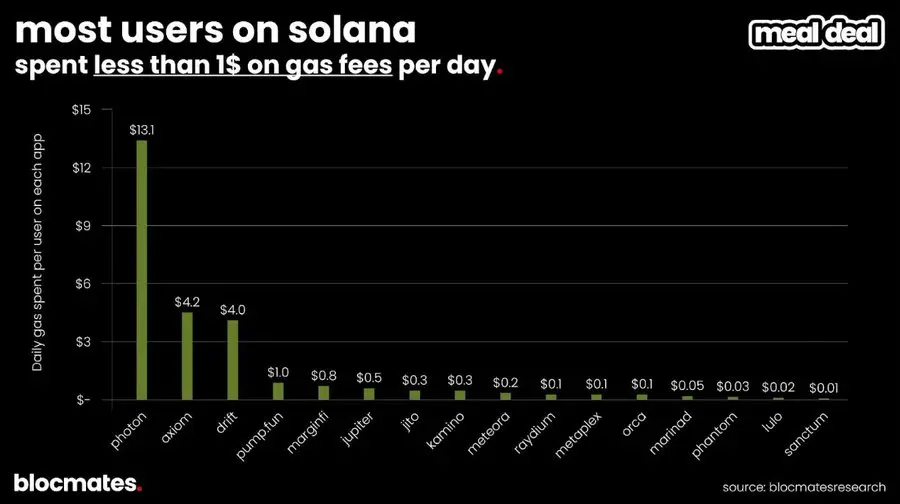

Although Solana has always been known for being “fast and cheap,” this does not mean there are no exceptions. For example, some high-frequency, deep users on trading platforms such as @tradewithPhoton or @AxiomExchange incur daily transaction fees far higher than expected.

However, for the vast majority of users, using the most common applications on Solana costs only a few cents per day.

Solana vs. Core Competitors: A Horizontal Comparison

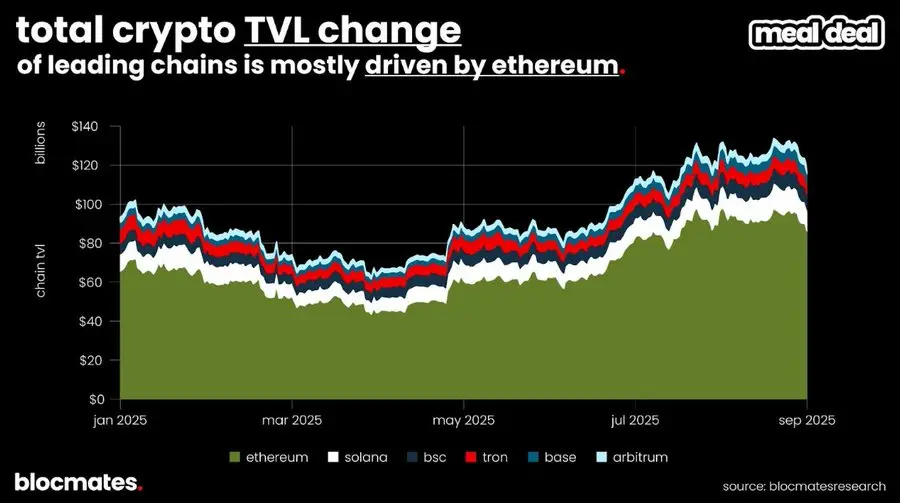

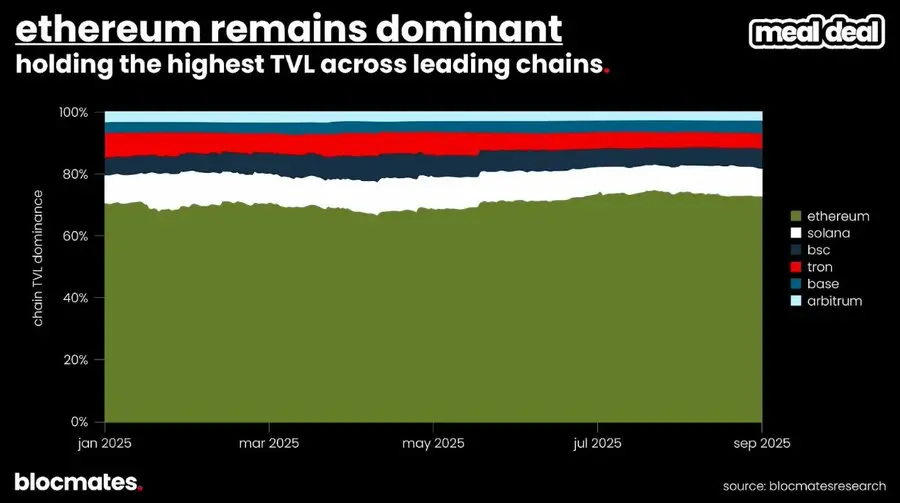

At the end of Q3, total chain TVL was slightly below the historical high of nearly $180 billions in 2021, but a horizontal comparison of competing public chains shows that their TVL quarter-on-quarter changes are actually quite limited.

The market share chart below clearly shows how the TVL of these competitors fluctuates in sync each week. As Newton said, “Idle capital tends to remain idle,” and once capital settles, it is often difficult to migrate on a large scale.

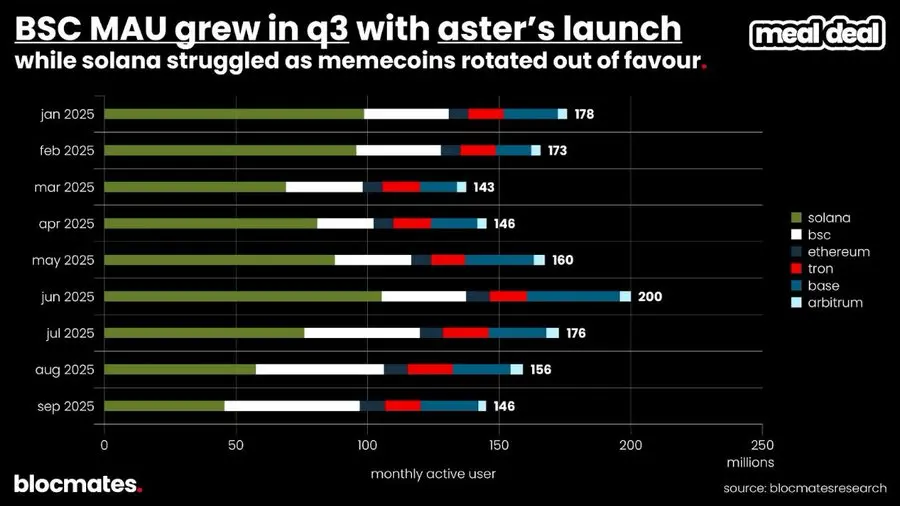

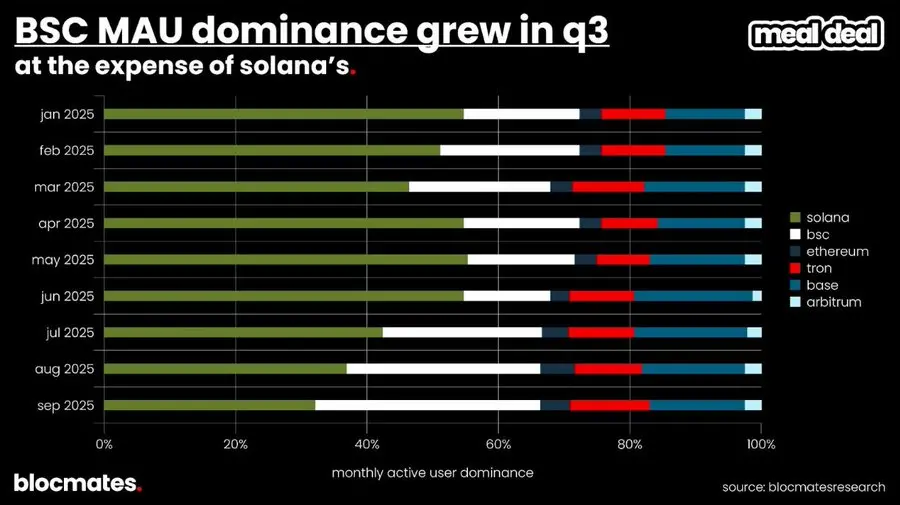

In terms of user scale, Binance Smart Chain grabbed the most attention in Q3 thanks to the perpetual DEX—Aster—associated with CZ. A large number of users either exited in early summer or migrated from Base and Solana to BSC.

Although Solana saw significant user growth in Q2, its share declined in Q3, almost in sync with the market’s waning interest in meme trading.

However, it is worth noting that, thanks to the surge in attention to stablecoins, Solana’s stablecoin supply has nearly tripled from the beginning of the year to the end of Q3. It turns out that “fast and cheap” is a major selling point for attracting users to stablecoins, especially given Solana’s already mature DeFi ecosystem.

Although these indicators depict the current landscape, they do not reflect the future direction. Solana’s identity has always been the “chain of experimentation.” To understand future use cases and narratives, we must observe which new experiments capital is flowing into.

VC Funding Flows: Which Projects Are Getting Funded?

Here are some Solana projects that received investment from well-known institutions in Q3:

- @raikucom: Completed a $13.5 million seed round in September 2025, focusing on real-time liquidity scheduling and cross-chain bridging DeFi infrastructure on Solana, mainly serving high-frequency trading applications, supporting sub-second settlement and avoiding MEV risks. The round was led by @PanteraCapital, with funds to be used for mainnet upgrades and further integration with DEXs (such as @JupiterExchange).

- @bulktrade: Completed a $5 million seed round in August 2025, a perpetual DEX for institutional users, featuring zero-gas batch execution with single trades up to $10 million. The round was led by @robotventures and @6thManVentures, with Solana co-founder @aeyakovenko also participating as an angel. Its alphanet testnet went live in Q3.

- @meleemarkets: Completed a $3.5 million pre-seed round in July 2025, a gamified prediction market protocol combining DeFi and social prediction, where users can earn yield-bearing tokens by making accurate predictions. The round was led by @variantfund and @dba_crypto, with funds for oracle integration and mobile launch. The project won second place in the Solana Breakout Hackathon.

- @hylo_so: Completed a $1.5 million seed round in September 2025, a decentralized stablecoin protocol on Solana supporting the issuance of yield-bearing stablecoins (such as sUSD) through over-collateralization and automatic rebalancing mechanisms. The round was led by @robotventures, with @SolanaVentures participating. Funds will be used for mainnet launch and integration with lending platforms such as @Kamino.

Where Are the Opportunities and Risks?

In Q3, Solana presented a state of “breakthroughs and burdens coexisting.” On the one hand, innovative applications are getting closer to product-market fit, and Digital Asset Treasury (DAT) companies are shining; on the other hand, the entire ecosystem has to face some thorny issues.

Outstanding Projects in Q3

Among the many dApps launched this quarter, the following projects stand out:

- @Titan_Exchange is a new DEX aggregator launched in Q3, using improved algorithms to extract depth from different liquidity pools with machine-level precision, thus obtaining the best quotes, outperforming existing similar products in 80% of cases.

- @DefiTuna is a new DeFi AMM launched in Q3, integrating a true on-chain limit order mechanism directly into the AMM design, avoiding security risks associated with off-chain matching, and allowing LPs to use up to 5x leverage for liquidity positions (leveraged yield).

- @xStocksFi tokenizes stocks held by licensed brokers, allowing crypto users to easily access the economic rights of underlying stocks; it launched at the beginning of Q3, with single-quarter trading volume exceeding $800 million (UTC+8) and a market share of about 60%.

- Pump.fun (streaming + mobile) launched a token buyback in Q3 after enduring heavy selling pressure, and relaunched its live streaming feature, with cumulative buybacks reaching $100 million (UTC+8) by the end of the quarter.

- @MetaDAOProject made headlines due to large-scale oversubscribed projects including Umbra. Projects launched through MetaDAO (see our report) bind legal, economic, and governance rights into their tokens, which are called “ownership coins.” In addition, its governance proposals are not decided by voting, but by trading in “futarchic markets,” allowing participants to express their views with real money.

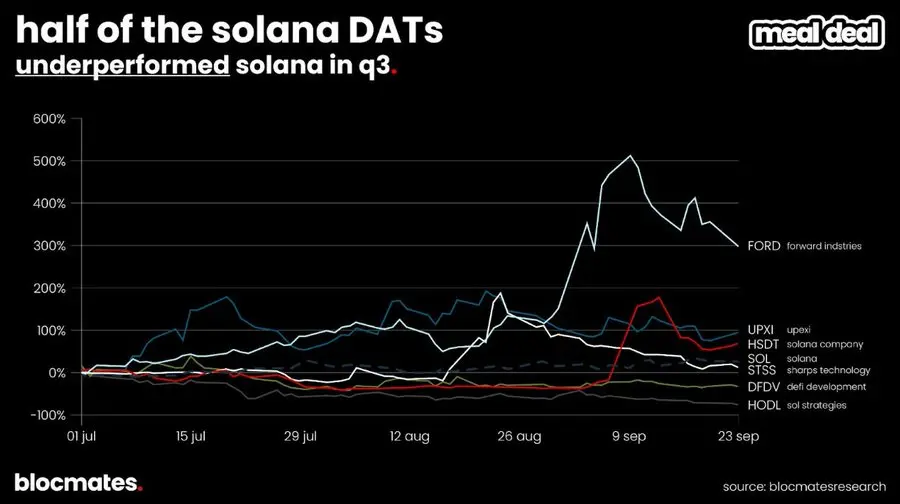

DAT Development

In Q3, Solana ecosystem DATs raised about $4.25 billions (UTC+8) through private placements, PIPEs, and equity offerings, with the largest being Forward Industries (FORD); about $3.5 billions was used to purchase 14.5 million SOL, accounting for 2.3% of SOL’s circulating supply.

Nevertheless, Solana DATs still faced the general mNAV contraction pressure seen in the crypto DAT ecosystem in Q3.

Responding to Common Criticisms

Like almost all crypto projects, Solana itself is in a continuous evolution stage and far from perfect. From our perspective, the following criticisms are more like inevitable growing pains, but they are still worth noting.

Biggest Risk: Brand Narrative

Solana has long been labeled as “the best place for experimentation.” Trading bots, ICM, consumer applications, AI agents—where did these innovations first appear? Solana.

But in this cycle, attention has become increasingly scarce, and projects that find product-market fit seem to be concentrated in only a few tracks and very few applications. This stagnation gives competitors a chance to seize the narrative:

- Perpetual contracts have migrated from general-purpose chains to application-specific chains like Hyperliquid;

- Base is betting heavily on consumer application narratives through Base app and Zora, which used to be Solana’s stronghold;

- Stablecoin chains such as Tempo, Plasma, Stable, and Arc continue to threaten Ethereum and Tron’s dominance in stablecoins.

This also leads to the core risk: Yes, Pump is a revenue machine and has indeed withstood competition from both “external” (Base/BSC) and “internal” (BonkFun) sources, but the side effect of this success is that it may permanently lock Solana’s brand as a “casino chain.”

To reverse this trend, Solana must drive new narratives. Maybe the answer is still Pump, but through its live streaming platform; maybe it’s the “non-ruggable ICO” and new governance structure proposed by MetaDAO; or perhaps it’s Toly’s personally styled, experimental solution aimed at Hyperliquid. The ecosystem needs new stories that can dilute the stigma brought by “second-level retail holders.”

Our Judgment on Solana’s Prospects

Although the market has been somewhat sluggish after the meme season ended, the significance of short-term price fluctuations is diminishing. Solana has established a solid position and is certain to exist for the long term.

The newly launched high-performance public chains (such as Sui, Aptos, Sei) have not posed a substantial threat to Solana as Solana did to Ethereum in the previous cycle. Even if some competitors are theoretically more advanced technologically, Solana is already “fast enough and cheap enough,” the user experience is good enough, and it supports a large ecosystem.

Technical capability and smooth experience are the foundation of adoption. Solana is not just maintaining its lead, but is continuously and rapidly iterating (see the upgrade section earlier in this report) to secure its position and expand its capabilities. For these reasons, developers still choose Solana as the high-performance chain of choice, and we believe this trend will not reverse.

Solana represents the crypto spirit of “daring to try, open competition, and extreme marketization,” and is the best arena for validating product-market fit. No matter where this cycle goes, Solana has the conditions to survive and continue to thrive. Even if some trading volume flows to application-specific chains, we still believe Solana will continue to lead in the general-purpose chain field.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Former Federal Reserve Governor Coogler faced an ethics investigation before resigning.

Nillion will gradually migrate to Ethereum.

Both gold and tech stocks have seen dip-buying, but only bitcoin remains "sluggish."

Compared with the capital inflows into tech stocks and gold's sharp rebound after a plunge, bitcoin was a clear exception in Friday's market: it defied the trend by dropping 5%, hitting a six-month low, and has now declined for three consecutive weeks. This contrast highlights the unusual situation in the bitcoin market: even as it maintains a high correlation of 0.8 with the Nasdaq 100 Index, bitcoin exhibits an asymmetric pattern of "falling more on declines and rising less on rallies." Meanwhile, intensified whale sell-offs and concentrated selling by long-term holders are jointly suppressing bitcoin.