The "Bankruptcy" of Metcalfe's Law: Why Are Cryptocurrencies Overvalued?

Currently, the pricing of crypto assets is largely based on network effects that have yet to materialize, with valuations clearly outpacing actual usage, retention, and fee capture capabilities.

Original Author: Santiago Roel Santos, Founder of Inversion

Original Translation: AididiaoJP, Foresight News

The Network Effect Dilemma of Cryptocurrency

My previous view that "cryptocurrency is trading at prices far above its fundamentals" sparked heated debate. The strongest objections were not about usage or fees, but stemmed from ideological differences:

· "Crypto is not a business"

· "Blockchain follows Metcalfe's Law"

· "The core value lies in network effects"

As someone who witnessed the rise of Facebook, Twitter, and Instagram, I know firsthand that early internet products also faced valuation challenges. But the pattern became clear: as users’ social circles joined, the product's value exploded. User retention increased, engagement deepened, and the flywheel effect was clearly felt in the experience.

This is the true manifestation of network effects.

If we argue that "cryptocurrency value should be evaluated from a network rather than a business perspective," then let's analyze it in depth.

Upon deeper investigation, an unavoidable issue emerges: Metcalfe's Law not only fails to support current valuations, but actually exposes their fragility.

The Misunderstood "Network Effect"

The so-called "network effects" in crypto are mostly negative effects:

· User growth leads to deteriorating experience

· Transaction fees soar

· Network congestion intensifies

The deeper issues are:

· Open-source nature leads to developer attrition

· Liquidity is profit-driven

· Users migrate across chains for incentives

· Institutions switch platforms based on short-term interests

Successful networks never operate this way; when Facebook added tens of millions of users, the experience never declined.

But New Blockchains Have Solved Throughput Issues

This does alleviate congestion, but it does not solve the essence of the network effect problem. Increasing throughput only removes friction; it does not create compound value.

The fundamental contradictions remain:

· Liquidity can leave

· Developers may move on

· Users may leave

· Code can be forked

· Weak value capture capability

Scaling improves usability, not inevitability.

The Truth Revealed by Fees

If L1 blockchains truly had network effects, they should capture most of the value like iOS, Android, Facebook, or Visa. The reality is:

· L1s account for 90% of total market cap

· Fee share plummeted from 60% to 12%

· DeFi contributes 73% of fees

· But accounts for less than 10% of valuation

The market is still pricing according to the "fat protocol theory," but the data points to the opposite: L1s are overvalued, applications are undervalued, and ultimately value will aggregate at the user aggregation layer.

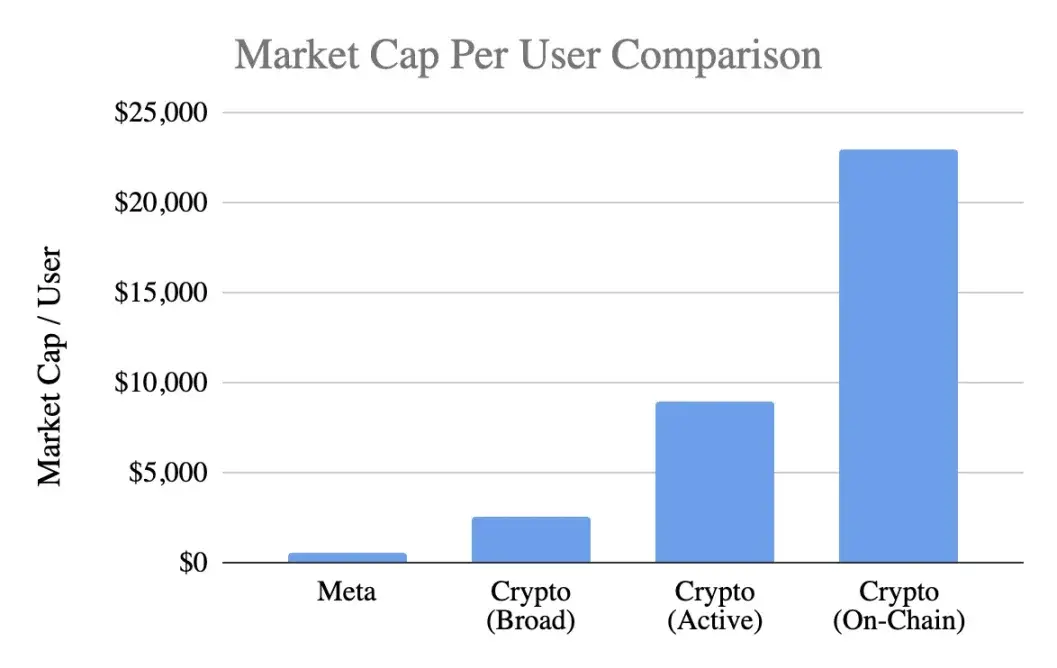

User Valuation Comparison

Using a general metric, market cap per user:

Meta (Facebook)

· 3.1 billion monthly active users

· $1.5 trillion market cap

· Per user value: $400-500

Cryptocurrency (excluding Bitcoin)

· $1 trillion market cap

· 400 million general users → $2,500 per user

· 100 million active users → $9,000 per user

· 40 million on-chain users → $23,000 per user

Valuation levels reach:

· 5x premium at the most optimistic estimate

· 20x premium under strict standards

· 50x premium based on real on-chain activity

Yet Meta is arguably the most efficient monetization engine in consumer tech.

On the Development Stage Argument

The argument that "Facebook was like this in its early days" is debatable. Although Facebook also lacked revenue early on, its product had already built:

· Daily usage habits

· Social connections

· Identity recognition

· Community belonging

· Value enhancement from user growth

In contrast, the core product of crypto is still speculation, which leads to:

· Rapid user influx

· Even faster churn

· Lack of stickiness

· No habit formation

· No improvement as scale increases

Unless crypto becomes "invisible infrastructure," a background service users are unaware of, network effects will be hard to self-reinforce.

This is not a maturity issue, but a fundamental product issue.

The Misuse of Metcalfe's Law

The law describes value ≈ n², which is appealing, but its assumptions are flawed:

· Users must interact deeply (rare in reality)

· The network should be sticky (actually lacking)

· Value should aggregate upwards (actually dispersed)

· There should be switching costs (actually very low)

· Scale should build a moat (not yet apparent)

Most cryptocurrencies do not meet these prerequisites.

Insights from the Key Variable k

In the V=k·n² model, the k value represents:

· Monetization efficiency

· Level of trust

· Depth of participation

· Retention ability

· Switching costs

· Ecosystem maturity

Facebook and Tencent's k values are between 10⁻⁹ and 10⁻⁷, tiny due to their massive network size.

Crypto's k value estimates (at $1 trillion market cap):

· 400 million users → k≈10⁻⁶

· 100 million users → k≈10⁻⁵

· 40 million users → k≈10⁻⁴

This means the market assumes each crypto user is worth far more than a Facebook user, even though their retention, monetization, and stickiness are all inferior. This is not early optimism, but excessive overdraw of the future.

The Reality of Network Effects

Crypto actually has:

Two-sided network effects (users↔developers↔liquidity)

Platform effects (standards, tools, composability)

These effects are real but fragile: easily forked, slow to compound, and far from the n² flywheel effect of Facebook, WeChat, or Visa.

A Rational View of Future Prospects

The vision that "the internet will be built on crypto networks" is indeed attractive, but it must be clarified:

1. This future may come, but it is not here yet,

2. The current economic model does not reflect it

Current value distribution shows:

· Fees flow to the application layer, not L1

· Users are controlled by exchanges and wallets

· MEV captures value surplus

· Forks weaken competitive barriers

· L1s struggle to solidify the value they create

Value capture is migrating from the base layer → application layer → user aggregation layer, which benefits users, but we should not pay a premium for it in advance.

Characteristics of Mature Network Effects

A healthy network should exhibit:

· Stable liquidity

· Concentrated developer ecosystem

· Improved base layer fee capture

· Continued retention of institutional users

· Growth in retention across cycles

· Composability defends against forks

Currently, Ethereum is showing early signs, Solana is gathering momentum, but most public chains are still far away.

Conclusion: Valuation Judgments Based on Network Effect Logic

If crypto users:

· Are less sticky

· Are harder to monetize

· Have higher churn rates

Their unit value should be lower than Facebook users, not 5-50 times higher. Current valuations have already priced in network effects that have not yet formed; the market is pricing as if powerful effects already exist, but in reality, at least for now, they do not.

Original link

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

When the Internet is Repriced: Interpretation of the Significance of x402

Is the four-year cycle of Bitcoin coming to an end?

Bitcoin breaks the Thanksgiving curse, returns to the $90,000 mark!

Altcoin ETF Acceleration Race: Six Months to Complete Bitcoin’s Ten-Year Journey