Ethereum Fundo Exodus: Has USDe150M Monthly Outflowed, But The Worst Is Yet To Come?

Scalability is facing a bottleneck, constrained by the "small and beautiful" nature of DeFi yield farming.

Original Title: "USDe Issuance Shrinks by $6.5 Billion, but Ethena Faces Bigger Challenges"

Original Author: Azuma, Odaily

Ethena is undergoing its largest funding outflow since its inception.

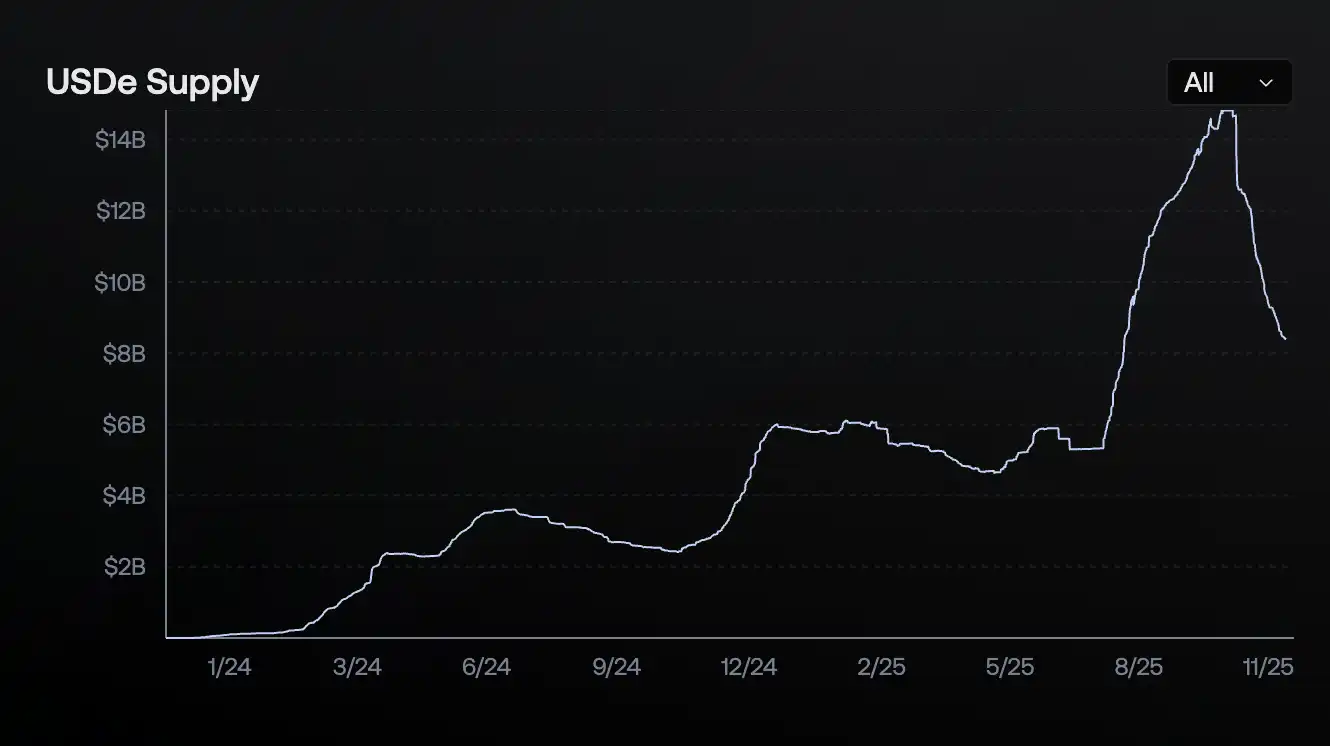

On-chain data shows that Ethena's primary stablecoin product, USDe's circulating supply, has dropped to 8.395 billion tokens, a reduction of approximately 6.5 billion tokens from its peak of nearly 14.8 billion tokens in early October. Although not quite a "halving," the decrease is still significant.

Coinciding with recent DeFi security incidents, especially two yield-bearing stablecoins, Stream Finance (xUSD) and Stable Labs (USDX), which claim to use a similar Delta neutral model as Ethena, collapsing in succession. Rumors suggest that the trigger for these collapses was the neutral balance breaking on October 11 due to CEX's ADL during the market crash, coupled with USDe's vivid memory of briefly deviating from its peg on Binance. Currently, there is a widespread FUD surrounding Ethena.

Is USDe Still Safe?

Given Ethena's current market size, if any unexpected event were to occur, it could potentially brew a black swan event comparable to Terra's back in the day... So, is Ethena in trouble? Is the fund outflow merely driven by risk aversion? Can you still confidently deploy funds into USDe and its derivative strategies?

Jumping to a conclusion, I personally tend to believe: Ethena's current strategy is still operating normally; while risk aversion in DeFi has exacerbated Ethena's outflow to some extent, it is not the main reason; USDe's current security situation remains relatively stable, but it is advisable to avoid leveraging too much.

The reason for acknowledging Ethena's current operational status mainly lies in two points.

Firstly, unlike most yield-bearing stablecoins that do not provide clear disclosures on position structure, leverage multiples, hedging exchanges, and liquidation risk parameters, Ethena can be said to be an industry benchmark in transparency. You can directly see reserve information and proofs, position distribution and percentages, implementation yield status, and other elements clearly on the Ethena website.

The second point is the issue of ADL mentioned earlier that causes imbalance in neutral strategy. There are rumors that Ethena has signed ADL exemption agreements with some exchanges, but this has never been confirmed, so let's not dwell on it for now. Even without exemption clauses, Ethena is essentially less susceptible to ADL impact. This is because from its public strategy, it can be seen that Ethena basically only selected BTC, ETH, and SOL as hedge assets (BNB, HYPE, XRP have a very small proportion), and these three major assets had relatively small fluctuations during the major crash on October 11. The counterparty's capacity to bear risks is also greater. ADL is actually more likely to occur in the highly volatile altcoin market where the counterparty's capacity to bear risks is smaller. Therefore, the ones that are most likely to suffer major losses at present are those protocols that are not transparent enough (possibly their strategy is too aggressive compared to the plan, or even not neutral at all).

As for the main reasons for the outflow of funds from Ethena, it can also be attributed to two points. First, as market sentiment has cooled down (especially after October 11), the basis arbitrage space between the futures and spot markets has narrowed, causing the protocol's yield and sUSDe annualized yield (as of the time of writing, it has dropped to 4.64%) to decrease simultaneously, making it less advantageous compared to mainstream lending markets such as Aave and Compound. As a result, some funds have chosen other paths for interest generation. Second, the price volatility of USDe on Binance on October 11 has raised market awareness of the risks associated with flash loans. In addition, the decrease in yields on both the off-chain (CEX subsidy reduction) and on-chain ends has led to a large amount of funds unwinding flash loans and withdrawing funds.

Based on the above logic, we believe that Ethena and USDe still maintain a relatively stable operational state. Although this round of fund outflows has exceeded expectations to some extent due to extreme market conditions and security incidents, the main reason can still be attributed to the decrease in attractiveness caused by the narrowing of arbitrage opportunities in a subdued market sentiment. This is precisely determined by Ethena's design logic—affected by market environment fluctuations, the protocol's yield and fund attractiveness will also fluctuate in sync.

A More Severe Test: Scalability

Compared to the phased outflow of funds, the even more severe issue facing Ethena is that its Delta-neutral model relying on the perpetual contract market seems to have reached a bottleneck in terms of scalability.

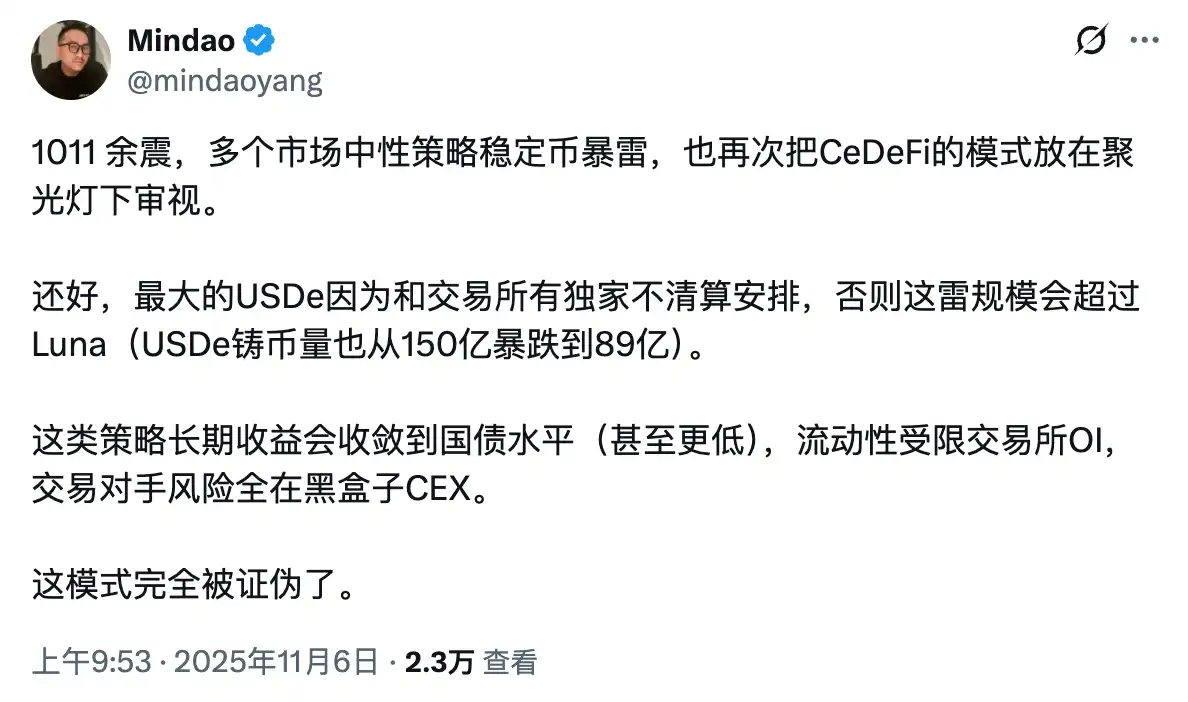

On November 6, DeFi expert Mindao commented on the recent stablecoin liquidity crisis related to the neutral strategy, stating: "The long-term returns of such strategies will converge to the level of government bonds (or even lower), with liquidity constrained exchanges' Open Interest (OI), and counterparty risks all concentrated in the black box CEX. This model has been completely falsified... They cannot scale and will ultimately only be niche financial products, unable to compete with fiat-backed stablecoins."

This is akin to "The Truman Show," where Ethena once thrived in a small, limited-scale world but was confined by factors such as perpetual contract market size, exchange liquidity, infrastructure, etc., while the targets Ethena aspired to challenge, USDT, existed in the unrestricted larger world outside. Perhaps this inherent environmental growth difference is the greatest challenge that Ethena faces.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin Updates Today: Is Crypto’s Intense Fear Signaling a Market Bottom or Just a Misleading Decline?

- Crypto Fear & Greed Index fell to 24, with Bitcoin consolidating between $103,000-$115,000 amid prolonged market anxiety. - Extended fear periods historically precede market bottoms, but traders warn the index often lags and misfires in volatile conditions. - Coinbase aims to stabilize markets with 24/7 altcoin futures, yet regulatory clarity and persistent ETF outflows remain critical factors.

Bitcoin News Update: Bitcoin ETFs See $2.96 Billion Outflow as November Optimism Wanes

- BlackRock's Bitcoin ETFs lost $523M in single-day outflows on Nov 17, marking fifth consecutive net redemptions totaling $2.96B for November. - Despite November's historical 41.22% Bitcoin price surge, ETF redemptions signal cooling institutional/retail demand with average investor cost basis at $89,600. - Michael Saylor's firm bought 8,178 BTC at $102k average price, while JPMorgan warned Bitcoin-heavy companies risk index delistings by 2026. - BlackRock's IBIT holds 3.1% of Bitcoin supply but NAV multi

Bitcoin Updates: ECB Advocates for Digital Euro While Bitcoin's Decline Faces Regulatory Barriers

- ECB President Lagarde reaffirmed Bitcoin's "worth nothing" stance, rejecting its inclusion in central bank reserves due to safety and regulatory risks. - Bitcoin fell below $90,000 (32% from October 2025 peak), mirroring April 2025's correction amid U.S. rate uncertainty and large holder sell-offs. - ECB prioritizes digital euro development, aiming for 2027 pilot and 2029 launch to enhance privacy and reduce reliance on foreign payment systems. - Despite short-term Bitcoin rebound (3.64% in 24 hours), an

Ethereum News Update: Altcoins Face Critical Juncture—December Turning Point May Spark Market Recovery or Downturn

- Altcoins like ETH, XRP , and ICP trade near critical technical levels as institutional investors monitor potential inflection points ahead of a possible December market rebound or collapse. - Ethereum remains fragile below key moving averages with RSI near oversold territory, while XRP faces a $2.07–$2.10 support test that could trigger further declines if broken. - Smaller-cap tokens show speculative activity amid consolidation, with ICP's $4.97 resistance and Bitcoin's $88,000 support level serving as