Bitget UEX Daily|US-Iran Deal Reached to Reopen Strait of Hormuz; SpaceX Surges 19% on Debut with Market Cap Exceeding $2 Trillion; Strong Asia-Pacific Markets, Japan and Korea Lead Gains

Bitget2026/06/15 01:35

Bitget2026/06/15 01:35

I. Hotspot Headlines

Federal Reserve Dynamics Fed Focuses on Treasury Yield Pressure and Policy Path

- Goldman Sachs trading head notes that if the 10-year Treasury yield reaches 5%, it could exert substantial pressure on stock valuations; although not yet breached, bond market volatility has intensified.

- Investors are watching the upcoming FOMC meeting closely, with the interest rate path facing repricing.

- Market Impact: Against the backdrop of AI-driven stock strength, rising Treasury yields may suppress risk assets. In the short term, attention should be paid to potential drag from the bond market on equity valuations.

International Commodities US-Iran Deal Eases Geopolitical Tensions, Weighing on Oil Prices

- Trump announced free passage through the Strait of Hormuz and the lifting of the naval blockade; the US and Iran signed a ceasefire memorandum of understanding, with the formal signing ceremony scheduled for June 19 in Switzerland.

- An Israeli airstrike triggered criticism from Trump, but the overall agreement reduces the risk of conflict escalation.

- Market Impact: The deal alleviates supply concerns, driving oil prices lower, which benefits risk assets but may suppress the energy sector.

Macroeconomic Policy G7 Summit Opens Amid Economic Data Focus

- The 52nd G7 Summit is underway in France, focusing on global economic coordination.

- Today’s releases include the US New York Fed Manufacturing Index, industrial production, and NAHB Housing Market Index.

- Market Impact: Data outcomes and summit results will influence Fed expectations and market risk appetite. Current geopolitical easing provides a relatively stable environment for policy discussions.

II. Market Review

Commodities Forex Performance

- Spot Gold: ~$4,300/oz, +2%.

- Spot Silver: ~$70/oz, +2.8%.

- WTI Crude: ~$80/barrel, -4.24%.

- Brent Crude: ~$84/barrel, -3.74%.

- Dollar Index (DXY): ~99.57 points, -0.23%.

Driver Analysis: The US-Iran ceasefire agreement has significantly eased geopolitical risks. Expectations of reopening the Strait of Hormuz have undermined fears of oil supply disruptions, causing sharp declines in crude prices. Gold and silver benefited from improved risk sentiment and relatively stable USD, posting rebounds. The DXY traded in a narrow range, reflecting market caution toward Fed policy balanced against geopolitical de-escalation. Overall asset correlations are evident: reduced geopolitical risk boosted equities and crypto but pressured energy prices. Gold, as a safe-haven asset, faced short-term pressure but retained support from industrial and investment demand. Institutional consensus suggests macroeconomic data and G7 outcomes will dominate near-term direction. If the inflation path remains benign, precious metals are expected to maintain resilience, while crude oil supply-demand rebalancing will hinge on implementation of the agreement.

Crypto Performance

- BTC: ~$65,500, +1.2%.

- ETH: ~$1,720, +1.9%.

- Total Crypto Market Cap: ~$2.32 trillion, +1.3%.

- Market Liquidations: 24h total ~$324 million, with shorts ~$230 million.

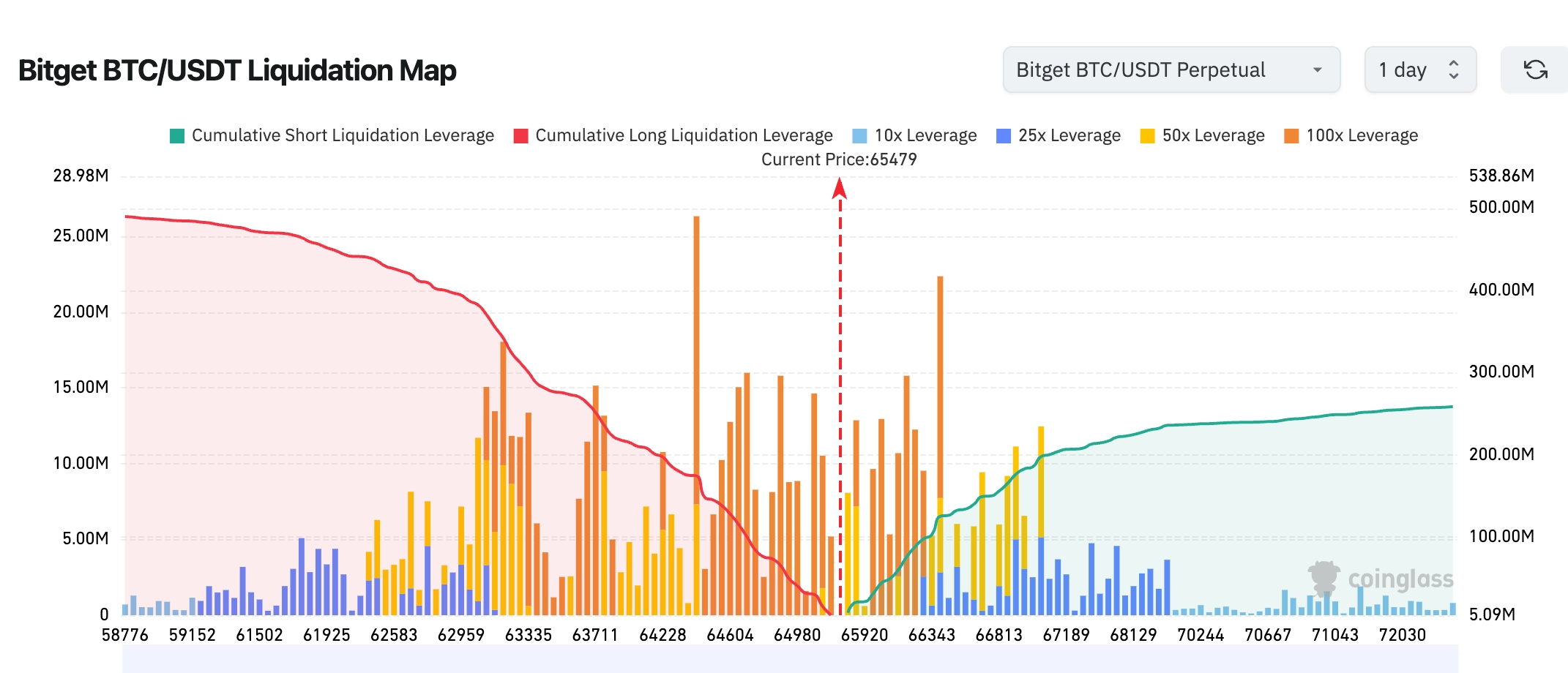

- Bitget BTC/USDT Liquidation Heatmap: At current BTC price of ~$65,479, long liquidation zones around $64,500–$65,000 have largely been cleared, significantly reducing short-term downside leverage pressure. Significant short liquidation clusters sit above at $66,300–$67,200; continued upside through $66,000 could trigger short covering and accelerate prices toward $67,000+.

- Spot ETF Net Flows: As of last Friday, BTC spot ETFs saw net inflows of ~$86 million.

Driver Analysis: The US-Iran deal eased geopolitical tensions and boosted risk appetite, while SpaceX’s successful debut provided positive spillover. BTC and ETH rebounded, market cap stabilized, and ETF flows turned modestly positive, easing prior outflows. Liquidations were dominated by shorts, indicating forced covering that supported prices. Technically, BTC is consolidating above $60,000. Institutions believe improved macro conditions and inflows will underpin near-term trends, though ETH remains relatively differentiated due to AI and Layer-2 narratives. Overall, sentiment has shifted from prior panic to cautious optimism, with focus on Fed policy and upcoming macro data for liquidity guidance.

US Stock Index Performance

- Dow: Closed ~51,202 points, +0.7%, extending upward momentum.

- SP 500: Closed ~7,431 points, +0.50%, showing steady characteristics.

- Nasdaq: Closed ~25,889 points, +0.31%, driven by technology and semiconductor sectors.

Tech Giants Performance

- NVDA: ~$205.19, +0.16%.

- AAPL: ~$291.13, -1.52%.

- MSFT: ~$390.74, +0.10%.

- GOOGL: ~$359.68, +0.53%.

- AMZN: ~$238.55, -1.23%.

- META: ~$566.98, -0.26%.

- TSLA: ~$406.43, +1.82%.

Summary and Driver Analysis: The tech giants sector largely moved with the broader market. SpaceX’s 19% debut surge and market cap exceeding $2 trillion boosted sentiment, with most semiconductors advancing (NVDA modestly higher). However, differentiation emerged: TSLA performed relatively strongly on positive catalysts, while AAPL and AMZN saw mild pullbacks. AI-related names benefited from valuation expansion, whereas some consumer tech names faced valuation pressure or company-specific adjustments. Events highlighted in the Futu briefing underscore ongoing space and AI enthusiasm, but caution is warranted regarding potential pressure from rising yields on high-valuation stocks.

Crypto Market Stock Contracts Overview

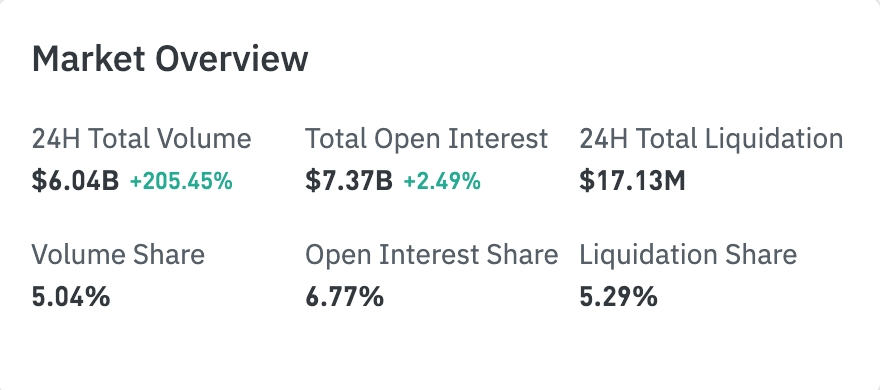

- Stock contract market activity surged noticeably, with 24H total turnover reaching $6.033 billion, up 204.94%.

- Total open interest rose to $7.358 billion (+2.39%), indicating continued capital inflows.

- 24H total liquidations of $17.1293 million remained relatively contained against sharply higher turnover.

Sector OI Performance

- Technology sector OI at $1.342 billion, far exceeding others and remaining the core trading focus.

- Financial sector OI at $160 million, ranking second.

- Consumer sector OI at $67.64 million, clearly ahead of industrials and biotech.

- Industrials ($24.96 million) and biotech ($13.07 million) saw relatively lower attention.

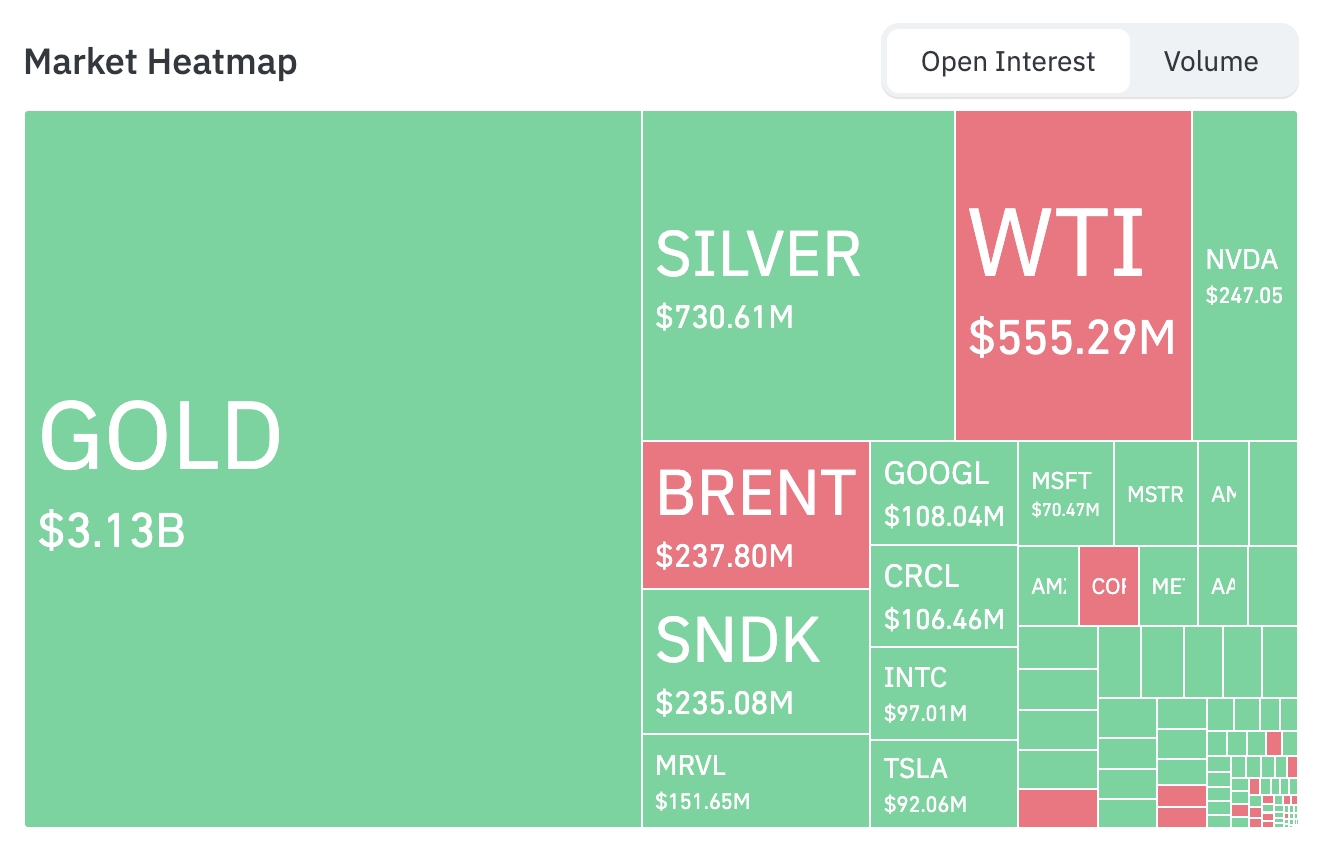

Heatmap Capital Distribution (by OI)

Commodities

- Gold (GOLD): RMB 3.125 billion – largest position, reflecting strong safe-haven demand.

- Silver (SILVER): RMB 728 million – second.

- WTI Crude ($556 million) and Brent Crude ($238 million) maintained notable positions but lagged precious metals.

Tech Stocks

- NVIDIA (NVDA): RMB 247 million – top tech holding.

- SanDisk (SNDK): RMB 235 million, Marvell (MRVL): RMB 152 million stood out, showing continued capital bets on AI storage and semiconductor chains.

- Google (GOOGL): RMB 108 million, Circle (CRCL): RMB 106 million – both over RMB 100 million.

- Intel (INTC): RMB 97.12 million, Tesla (TSLA): RMB 92.07 million retained high attention.

Sector Movers Observation Semiconductor Sector Mostly Higher but with Notable Differentiation

- Representative names: ARM +11%+, Seagate +7%+, Intel/Western Digital +6%+, SanDisk +5%+, AMD/Qualcomm +4%+; Micron slightly down ~1.4%.

- Drivers: Sustained AI memory and chip demand supported overall sector performance, but individual fundamentals diverged due to supply chain dynamics, valuation adjustments, and company-specific news.

Media/Consumer Tech Sector Moves

- Representative name: Roku Inc (ROKU) +20%, largest single-day gain since November 2023.

- Drivers: Rumors of potential sale talks, combined with improved overall risk sentiment, drove strong rebound.

Aerospace/Emerging Tech Sector Outbreak

- Representative name: SpaceX (SPCX) +19% on debut, turnover ~$80 billion, market cap exceeding $2.1 trillion.

- Drivers: As a space leader, its record-breaking IPO not only set new benchmarks but also boosted investor confidence in high-growth tech tracks; Cathie Wood’s ARK heavy buying further amplified enthusiasm.

Software Sector Pullback

- Representative name: Adobe (ADBE) -6.7%, worst single-day performance in recent period.

- Drivers: Company-specific developments or broader concerns over software growth sustainability weighed on sentiment, highlighting intra-sector differentiation.

III. Individual Stock In-Depth Analysis

1. SpaceX (SPCX) – IPO Debut Event Overview: SpaceX made its Nasdaq debut, opening above the $135 issue price with relatively contained intraday volatility, ultimately closing up 19% near $161, pushing market cap past $2.1 trillion and ranking it among America’s top six companies. Volume exceeded 500 million shares with turnover around $80 billion, setting multiple IPO records. Cathie Wood’s ARK Invest acquired ~3.29 million shares privately for ~$443 million, making SpaceX the top holding in its Venture Fund. Options trading begins next week, further enhancing liquidity and hedging tools. The massive raise (approximately $75 billion) at a near-$2 trillion pre-IPO valuation saw further expansion post-listing, underscoring strong investor conviction in the long-term prospects of the space economy. Market Interpretation: Wall Street institutions broadly favor SpaceX’s technological moat and commercialization potential as a leader in space exploration and satellite internet. Despite elevated valuation, its dominance in Starlink and Starship projects is viewed as a long-term growth engine. The smooth listing also eased concerns over liquidity strain from a wave of mega-IPOs. Investment Insight: SpaceX’s debut sets a benchmark for emerging tech tracks, with near-term示范效应 likely spilling over to related chains. However, high valuation warrants caution against profit-taking. Monitor subsequent earnings, contract execution, and options market dynamics for entry timing.

2. Adobe (ADBE) – Sharp Decline Event Overview: Adobe fell 6.7% in a single session, its worst performance since March, with elevated turnover. The market linked this to recent company developments and broader software valuation reassessment pressure. While no single event fully dominated, the defensive weakness of software within tech rotation contributed to the adjustment. Market Interpretation: Analysts argue that amid AI investment fervor, valuations of some traditional software giants have decoupled from fundamentals, prompting questions around growth sustainability and capital returns. As a creative software leader, Adobe continues investing in AI features but faces near-term cost pressures and intensifying competition, leading to cautious sentiment. Investment Insight: Short-term volatility offers a watching window. Focus on next-quarter AI monetization data and management guidance; stabilization in fundamentals could present medium-term entry opportunities.

3. Roku (ROKU) – Strong Rebound Event Overview: Roku surged ~20%, its largest single-day gain since November 2023, accompanied by significantly higher volume. Market rumors of potential sale or strategic transaction talks, combined with improved risk appetite, drove rapid recovery from recent lows. Market Interpretation: Institutions view Roku as a key infrastructure provider in streaming, with a moat in advertising and content distribution. In a consumption recovery environment, potential acquisition premium serves as a key catalyst. Investment Insight: Event-driven moves suit short-term trading, but watch for rumor verification risks. Monitor official statements and industry consolidation progress.

4. Sivers Semiconductors (SIVE) – AI Optics Collaboration Event Overview: Sivers Semiconductors deepened silicon photonics collaboration with GlobalFoundries for AI data center co-packaged and pluggable optics solutions, while securing an ~$8.2 million Ka-band beamforming IC production order from All.Space. Despite Q1 revenue decline and expanding operating losses/cash burn, order pipeline and strategic alliances boosted sentiment, leading to notable volatility and staged rebounds. Market Interpretation: Analysts recognize its technological expertise in AI infrastructure optical interconnects. Successful capacity expansion and CHIPS Act support could materially improve long-term growth trajectory, though near-term execution risks and valuation swings require attention. Investment Insight: Well-suited for AI supply chain thematic allocation. Evaluate positions based on order execution progress and monitor potential dual-listing benefits for liquidity.

5. AXT Inc. (AXTI) – Indium Phosphide Shortage AI Demand Event Overview: AXT experienced sharp price swings recently, fueled by reports of potential indium phosphide export restrictions and surging AI data center material demand. Analysts raised price targets multiple times. The company is actively expanding capacity, with Q1 showing improved gross margins and a $100 million backlog. Despite governance issues and financing activities, AI-driven demand prospects remain the core catalyst. Market Interpretation: Institutions believe AXT’s position in semiconductor substrates, particularly indium phosphide, will directly benefit from data center and 5G/6G expansion, though geopolitical export risks represent the primary uncertainty. Investment Insight: Medium-term constructive on AI materials theme. Monitor capacity milestones and geopolitical policy developments; manage position sizing given high volatility.

IV. Views Developments

- Brian Armstrong posted on X that his bullishness on Bitcoin remains unchanged and he maintains a long-term long position, noting that things are never as good or as bad as they seem.

- Serenity stated that technical analysis (TA) is more like traders’ “astrology” — essentially a combination of confirmation bias and market psychology used to gauge sentiment rather than determine core price drivers. Sharp rises in multiple stocks stem not from chart patterns but from fundamentals and expectations. For example, SIVE’s ~1,900% surge reflects market repricing of future revenue tied to JBL and GFS; AXTI’s ~8,000% gain links to indium phosphide substrates, photonics demand, and export controls. Serenity added that TA mainly captures participants’ psychological expectations (e.g., chart-based predictions for IREN cannot offset structural supply pressure from large ATM financing). True drivers of stock trends should include industry thematic linkages, earnings expectation changes, macro environment, financial performance, and float structure. TA may help time entries, but long-term upside depends on fundamentals and capital structure rather than “chart faith.”

- Tokenized Pokémon cards are seeing rapid trading volume growth on crypto platforms. Driven by “gacha” mechanics, physical cards are mapped to NFTs or digital credentials, creating box-opening/draw experiences. Messari data shows ~$230 million in trading volume across Solana, Polygon, Base, BNB, and five other blockchains in May — roughly 10x growth year-over-year.

- Pakistani Prime Minister Shehbaz announced on Sunday that the US and Iran have declared an end to hostilities. Both sides are expected to hold a formal signing ceremony this Friday (June 19) in Switzerland, followed by more detailed nuclear negotiations. Shehbaz posted on X: “A peace agreement between the United States of America and the Islamic Republic of Iran has been reached. Both parties have announced an immediate and permanent cessation of military actions on all fronts (including within Lebanon).” He added that the agreement “is now in effect.” Trump confirmed the news, stating he is lifting the US blockade and expects Iran to open the Strait of Hormuz. Iran has also responded.

- According to Xinhua, Britain, France, Germany, and Italy issued a joint statement saying that after the US-Iran agreement to end the war, parties are prepared to lift relevant sanctions on Iran in exchange for steps on its nuclear program.

- Analyst Darkfost posted on X that on-chain behavior of Bitcoin long-term holders (coins held >6 months) still shows “phased high-intensity selling” with exchange inflows significantly above annual averages (up to 5x). Short-term, LTHs continue transferring BTC to exchanges, implying ongoing selling pressure, typically corresponding to actual sales. Long-term, however, average annual LTH inflows to exchanges are declining, indicating a preference for holding. Recent data shows a modest rebound from ~630 BTC/day in early May to over 800 BTC/day, but still at historically low levels since 2015. This may relate to rising ETF and institutional ownership altering holder structure, but overall systemic selling pressure from LTHs on medium- to long-term markets is diminishing.

V. Today’s Market Calendar

Data Release Schedule

| 20:30 | US | New York Fed Manufacturing Index | ⭐⭐⭐ |

| 21:15 | US | Industrial Production MoM | ⭐⭐⭐ |

| 22:00 | US | NAHB Housing Market Index | ⭐⭐⭐ |

-

US Economic Data: Empire State Manufacturing Index, May Industrial Production, etc. Focus on signals of manufacturing recovery.

-

Earnings: A number of small-to-mid cap companies reporting pre-market or after-market (no major heavyweights this week).

-

US Economic Data: Import Price Index, May Housing Starts & Building Permits, etc. Watch for inflation pass-through and housing market trends.

-

Earnings: Wiley (WLY), La-Z-Boy (LZB), etc.

-

US Economic Data: May Retail Sales (focus on consumer resilience). ★★★★

-

Federal Reserve FOMC Interest Rate Decision and Economic Projections (Kevin Warsh presiding over his first meeting as Chair): Markets widely expect rates to remain unchanged (currently around 3.75%). Key focus will be on Warsh’s tone at the press conference, comments on inflation and employment, and any signals regarding potential future rate hikes. ★★★★★

-

Earnings: Jabil (JBL), etc.

-

US Economic Data: Initial Jobless Claims for the week of June 13, Philadelphia Fed Manufacturing Index, etc.

-

Earnings: Accenture (ACN), Kroger (KR), etc. — key focus (consumer and technology services sectors). ★★★★

-

US markets closed for Juneteenth federal holiday .

Institutional Views: Prominent investment bank analysts generally believe the US-Iran agreement has significantly improved risk sentiment, boosting equities and crypto, while lower oil prices highlight supply-demand rebalancing. SpaceX’s successful listing has lifted tech confidence, though Goldman Sachs warns that Treasury yields nearing 5% could create pressure. In crypto, modest ETF inflows and liquidations support near-term rebounds; institutions favor BTC consolidating in the current range but emphasize that Fed policy and macro data will determine second-half direction. The overall market has entered an observation phase. Pay attention to G7 and economic data for liquidity guidance, and focus on asset correlations and valuation differentiation.

Disclaimer: The above content is compiled by AI search with manual verification only for release. It does not constitute any investment advice. Data in the text inevitably contains deviations; please refer to real-time market data.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Trump’s Post Shocks the World! U.S.-Iran Deal in Sight as Oil Plunges and Asian Stocks Rally

Japanese Yen flatlines on US-Iran deal, BoJ rate hike expectations

The Funding: Is the bitcoin bottom in? Crypto funds weigh in

Canadian Dollar rises as US Dollar declines on fading safe-haven demand