3 Key Motives to Sell SOLV and One Alternative Stock Worth Buying

Solventum Stock Performance: Recent Trends and Investor Concerns

In the last half-year, Solventum’s share price slipped to $67.18, resulting in a 6% loss for investors. This decline stands in contrast to the S&P 500’s 2.6% gain during the same period, leaving many shareholders questioning their next move.

Should you consider adding Solventum to your portfolio, or does it pose unnecessary risk?

Reasons We’re Cautious on Solventum

Despite the lower price point, we’re choosing to stay on the sidelines for now. Here are three key factors behind our decision, along with an alternative stock we prefer.

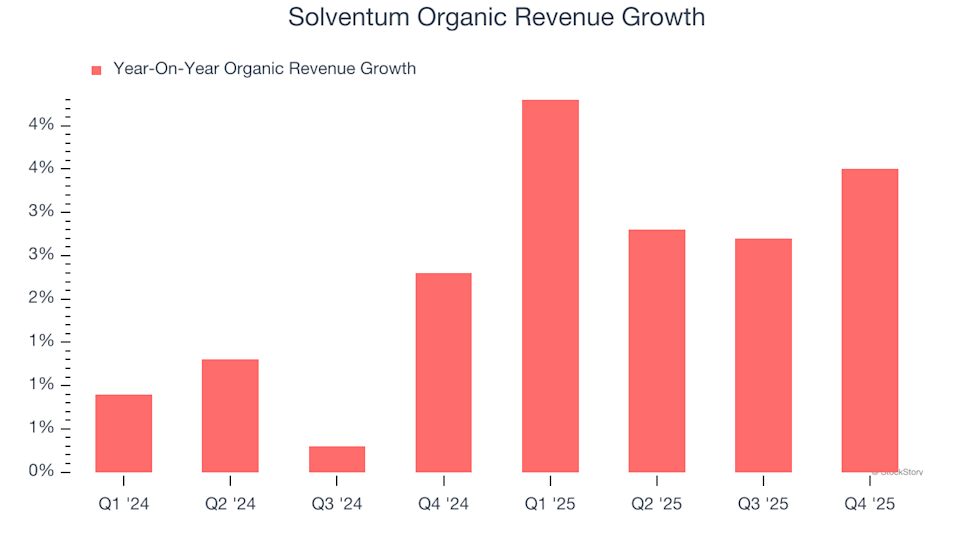

1. Organic Growth Remains Weak

To gauge the health of companies in the Surgical Equipment & Consumables sector, organic revenue growth is a crucial indicator. This measure strips out the effects of mergers, acquisitions, divestitures, and currency changes, offering a clearer view of the core business.

Solventum’s organic revenue has grown at an average annual rate of just 2.3% over the past two years, trailing behind industry peers. This sluggish pace suggests the company may need to enhance its offerings, pricing, or sales approach—potentially complicating its operations further.

2. Declining Earnings Per Share

Tracking long-term changes in earnings per share (EPS) helps reveal whether a company’s additional sales are translating into real profits. Sometimes, revenue can rise due to heavy marketing spend rather than true business growth.

Unfortunately, Solventum’s EPS has dropped by an average of 31.6% per year over the past three years, while revenue has remained stagnant. This pattern indicates the company has struggled to adapt its fixed costs to fluctuating demand.

3. Shrinking Free Cash Flow Margin

Free cash flow, which accounts for all operational and capital expenditures, is a telling metric that’s difficult to manipulate. It’s a vital sign of financial health.

Over the last four years, Solventum’s free cash flow margin has fallen by 26.7 percentage points. If this trend persists, it could point to rising investment requirements and greater capital intensity. For the most recent twelve months, the company’s free cash flow margin was essentially zero.

Our Verdict

Solventum does not meet our standards for a high-quality investment. After its recent decline, the stock trades at a forward P/E of 10.1 (or $67.18 per share), which is a reasonable valuation. However, we remain unconvinced about the company’s prospects and believe there are stronger opportunities elsewhere. We suggest considering a reliable industrials company benefiting from ongoing industry upgrades as a better alternative.

Top Stocks for Any Market Environment

Don’t Miss: The Top 5 Momentum Stocks. The ideal moment to invest in a standout stock is when the market starts to recognize its potential. These companies not only have solid fundamentals but are also experiencing strong momentum right now.

Discover which stocks our AI-driven platform is highlighting this week.

Our selections have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Comfort Systems, which delivered a 782% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Insight Wealth Has Acquired an Initial $26.9 Million Position in VPLS

BNB Price Reclaims 4th Place From XRP — Analysts Eye $900

Recognizing Bottoms earlier. Identifying Earnings before gaps.

SNDK: Something Big Is Happening Before the Nasdaq-100 Add